Treasurers have been keeping a keen eye on the financial press of late, and for good reason. It seems that not a week goes by without one of the world’s banking institutions announcing either staff cuts, a restructuring, the closure of their business in a certain market or, in some very high-profile cases, a nearly complete exit from certain lines of banking all together.

This is perhaps not that surprising; after all, it has been an especially challenging time for banks around the world. In the wake of the global financial crisis, banks have been bailed out by governments, seen credit ratings decline and also been hit with a glut of regulation. Combined, these factors are limiting the ability to act as they once did.

But banks are not only being pressured by the regulators. In recent years, technology has progressed to the stage where non-traditional players can enter the financial industry, offering products and services that can sometimes go above and beyond those offered by established financial institutions. In the retail space, payments and funding are two prime examples of where these fintech firms are having a big impact and disintermediating banks, and there is no reason why this couldn’t happen in the corporate sphere.

Despite all these changes, one statement remains true: corporates need banks, just as much as banks need corporates. A bank remains a critical counterparty to any corporate operation and a key tool in ensuring the business operates smoothly, day-to-day. But the recent changes in the financial services industry has certainly placed a renewed focus on bank relationships and the risk these can pose to the business. And it is very likely that this will only intensify and evolve over the coming years.

Seeing banks differently

It is not an exaggeration to say that the global financial crisis changed everything when it comes to the banking sector and how it is perceived by corporate treasurers. As Ricky Thirion, Group Treasurer at Etihad Airways outlines, the biggest change for treasury in the wake of the crisis, has been around how Etihad perceives the safety of its counterparties, especially the banks.

“As you enter into a global crisis, you ask yourself fundamental questions about risks you are facing, especially with financial institutions where it profoundly changed people’s views on credit risk,” he says. “I think for many of us that will, in our lifetimes, be the biggest thing we remember about that time.”

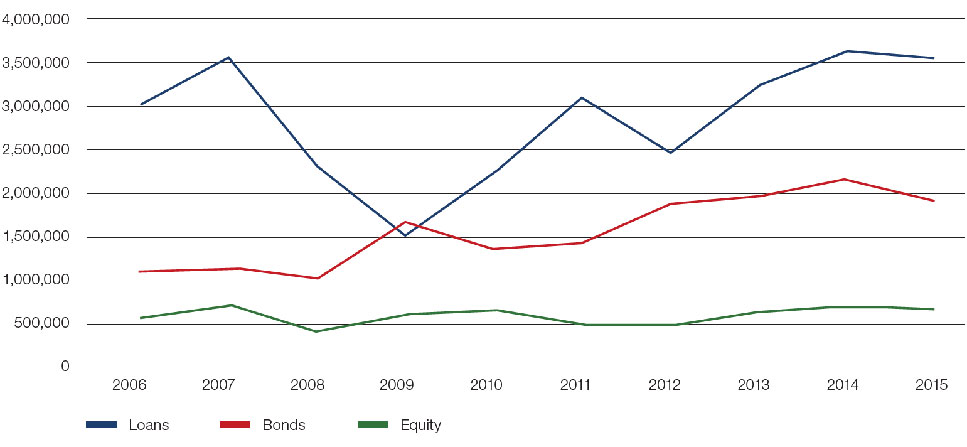

Indeed, the crisis provided a severe wake up call to corporates with regards to the over-reliance that many had on their banks for funding. The larger names, almost instantly, began to diversify their funding strategies and other companies soon followed. This point is highlighted by the below chart taken from the 2016 Allen & Overy Corporate Funding Monitor study. As it clearly depicts, during the years of the crisis, bank lending fell dramatically, whilst bond issuances increased. More recently, however, bank lending has increased, returning to pre-crisis levels in 2015 – at the same time bond issuances have also steadily increased.

Chart 1: Despite volatility and complexity, corporates continue to have funding options

Corporate funding – by source global (USDm)

Source: Allen & Overy Corporate Funding Monitor study 2016

Yet, Craig Kennedy, Partner at EY, is keen to point out that despite the recent increase in bank led funding this doesn’t mean that there has been a return to the status quo. “Corporates are now obtaining their funding from broader, more diverse sources,” he says. “Moreover, in many cases, funding isn’t provided as traditional loans but rather through alternative products such as supply chain finance.” Indeed, this nuance is highlighted in the study which states: “Companies (in 2015) found they could raise money more cheaply and in more ways than ever before. The new normal that is emerging for corporate funding is a lot more complex than it used to be, but it’s working.”

Evolving expectations

However, it is not just funding dynamics that have changed for corporates. The whole spectrum of what corporates expect from their banks and the price that they are willing to pay for this has also altered.

To highlight this, David Kelin, Director, Academy at treasury consulting firm Covarius, outlines how in the days before the crisis the banking sector was largely homogeneous and commoditised, particularly in respect of the global banks and the products and services they offered. Price, therefore, was often the main differentiating factor.

Today, this has changed significantly. “Corporates are using a multitude of different selection criteria that goes much deeper than pricing,” says Kelin. “Banks today are quite different from one another in terms of what they can offer, so corporates are looking to see if the banks can provide suitable credit, if the bank has a sophisticated product suite, if it is committed to certain markets and the business more broadly and so forth.”

Price, of course, remains important, but there is a willingness to pay more should they excel in the areas important to the corporate. “No corporate will say they will pay more to their banking partner, but I have worked with clients recently who have paid more for a service simply because they thought the bank offered much more in other areas, or was the only bank offering that service,” adds Kelin. “This is a complete change from the pre-crisis days.”

Michelle Dovey, former Director of Treasury at Informa, echoes this point: “I think that value is important. For those companies outside of the top tier, it is necessary to conduct a robust cost-benefit analysis to ensure that you are getting the best deal for your money. I wouldn’t necessarily always select the cheapest provider, if I didn’t think their offering could live up to expectations.”

What is it therefore that corporates expect? For Dovey, her key expectation is for the bank to be loyal and look to forge a strong working relationship with her company. Making reference to the changing business plans of banks she says: “I want to work with a bank that will be there for us in the long-term and who understands our business and the direction we are heading in. This is an absolute must in today’s environment.”

Of course, the products and services that the banks offer are also important and Lesley Rogers, Regional Treasury Manager EMEA at AT&T, lists other criteria that must be delivered which include: robust products and offerings, a host to host facility; competitive tariffs and products to help reduce charges; electronic banking capabilities which are secure and have self-administrative offerings; one team for global documentation and customer services that are responsive and act in a timely fashion. Robust digital security has also been noted by treasurers as being an ever important consideration.

Yet, in similar fashion to Dovey, it is a relationship and honest two-way communication that is the key criteria for any bank wanting AT&T’s business.

Case study

Brocade Communication Systems – Scoring your banking partners

Being open and forthright with your banking partners can be challenging if the internal mechanisms for evaluating these are not well developed. Here Brocade outlines how it solved this challenge and derived numerous benefits from creating greater effectiveness around evaluating and communicating with its banking partners.

In the past, the relationships between Brocade and its banking partners were less than optimal. The existing process for bank relationship management was not structured, nor was it comprehensive. In fact, the evaluations on banking partners were mainly produced from fragmented feedback among the treasury staff.

Chris Hanson, Assistant Treasurer, explains: “Brocade was not able to effectively assess overall connections between our banking partners and establish meaningful bank relationships.” As a consequence, the other business units in Brocade could not properly select the right banking partners for their specific needs because they were lacking an accurate assessment on their banks. The following issues needed to be addressed:

Lack of systematic tracking of corporate banking expenditures vs revenues received from each banking partner.

The gap between how treasury views their banks and how business owners view their banks.

Evaluation’s scope was limited to treasury, other stakeholders were not involved.

Lack of effective communications between Brocade and banks when it comes to performance issues or improvement areas.

Inconsistent documentation with regard to overall performance of banking relationships.

Lack of tools to evaluate and enhance bank relationships.

The scorecard solution

In 2014, Brocade’s treasury established a bank relationship scorecard – an internal tool to determine strengths and weaknesses of each bank. Within the scorecard, specific cash management services by each banking partner were categorised into groups including bank products and customer services, capital management, administration, pricing, geographical footprint, and banking technology. The treasury staff graded the banks on a sliding scale from one (below expectation) to five (above expectation) and final scores were then calculated. Any time, if a bank rated below satisfactory, detailed reasons were given on a separate summary report. The results were communicated to the banks for follow-ups and improvements. Ultimately, it significantly improved bank services and relationships, resulting in higher customer satisfaction.

Angie Qian, Senior Treasury Analyst, explains: “we used the tool to communicate with our banks regularly. It helped to objectively communicate positive and negative feedback and supporting documents to our banking partners. Our banks appreciate our candid feedback and re-committed when necessary to improve their services and pricing where possible.”

Furthermore, treasury developed a wallet distribution model to analyse banking expenditures and revenues with each banking partner. The wallet distribution is an effective tool to provide the company insight into the expense and revenue expectations of a specific banking partner. It facilitates quicker decision making around selecting the right partnership for major services such as debt refinancing and stock repurchases. The company is now confident that the decisions made involving banking partners maximise all of their banking relationships.

Relationship results

The treasury team was able to conduct intensive reviews and evaluations of its banking processes because of this holistic banking relationship solution. The successful rollout of the scorecard and wallet distribution was achieved within a short period of time. The solution enabled Brocade to quickly eliminate one of their domestic banking partners and enhance international bank structures, resulting in $300k annual savings in bank fees. It also played a key role in selecting the right banking partner for a cash management optimisation project.

Treasury’s leadership at Brocade in innovating a comprehensive scalable global banking relationship management solution has improved all areas of the organisation. Brocade’s treasury is changing the way the company is thinking about the banking relationships, by getting all areas of the company to work together proactively evaluating and managing their banking partners. “Our goal is to implement a creative and efficient solution that leads to optimal decisions and results for the business,” notes Hanson.

Relationships or partnerships?

It is clear that corporates are calling for a relationship with their banking partners, but this is a fairly abstract term with multiple meanings. So, on a granular level, what is it that treasurers are expecting from this relationship?

For Chris Donohoe, Assistant Treasurer, Ingersoll Rand Plc. he is expecting the banks to understand his operations and objectives and work with him to meet these. As he highlighted last year at an industry conference, too often banks are coming to him with off-the-shelf products that don’t really meet the needs of a complex business. “What I’d like to see,” he added, “is banks taking the time to really get to know us.” Donohoe hoped that banks would then be in a better positon to offer a more educational approach when interacting with their clients, enabling treasurers to get the most effective use of a solution.

This point was echoed at the conference by Adam Boukadida, Deputy Treasurer at Etihad Airways, who said: “Banks have to understand our business and become a strategic partner rather than just looking at us as a sales opportunity.” With Etihad operating in more than 75 countries it has a complex business approach; banks must be able to understand the fundamental processes of their clients’ businesses as well as its technical treasury function.

Based on these statements, it seems that corporates are perhaps looking for more than just a relationship and are asking for the bank to be a business partner, almost akin to an extra member of staff in the treasury.

Delivering on expectations

Indeed, banks are recognising this need and in recent years many have pushed forward their advisory capabilities with similar gusto to their products. But market realities can sometimes curb even the best of intentions and the aforementioned regulatory burden under which the banks are currently operating is, in many cases, limiting their ability to offer the necessary products and services, let alone be a strategic partner to the business. As EY’s Kennedy points out: “Banks are altering the services they provide to their corporate clients. And some are pulling out of certain services and/or areas even when there is significant client demand.”

Kennedy goes on to highlight how, in recent months, he has had conversations with numerous treasurers who have found that no bank is willing to offer them a certain product or support them in a certain area. “This is not because there is something wrong with the corporate client, it is because there is simply nobody providing these services anymore.”

I want to work with a bank that will be there for us in the long-term and who understands our business and the direction we are heading in. This is an absolute must in today’s environment.

Michelle Dovey, former Director of Treasury, Informa

This has also been a trend noted by Dovey. “There is less choice for treasurers today,” she says. “Banks are retreating into the same products and markets where they make the most money whilst taking on the least risk.” She provides US private placements as an example of this trend. “Before the crisis, this was purely the domain of the US banks. Now every bank is pushing this product, whilst, on the other hand, there are very few banks now offering European cash management solutions.”

This is, of course, a big issue for corporates. “The treasury and cash management operation is business critical,” says Kelin. “And if a bank pulls out, it creates numerous issues around payments and collections, which the business is dependent on. As a result, even rumours of a bank pulling out puts fear into corporates and may make them take a closer look at their banking group.”

Managing the relationship

Taking a closer look at banking groups is, in fact, something that many corporate treasury departments are currently doing and many are switching. As a study produced earlier this year found, the key challenge for European treasurers in 2016 has been finding a new banking partner.

If you are a corporate treasurer with a stable banking group at present, you may be the envy of your peers. But, this is not a time to rest on your laurels, as shocks do happen. So how best can corporates and banks come together to create a healthy long-term relationship?

For Covarius’ Kelin, the key is communication. “Whilst corporates are demanding that their banks be honest with them, banks are also wanting to have frank and honest discussions with their clients to better understand their strategy. Given the limitations placed on banks at this present time this is important to ensure that they continue to offer the right products and services to each individual client. I don’t think banks are afraid to say ‘we can no longer help you’ anymore.”

Also, being open and honest can have additional benefits. Kelin, for instance, has had numerous conversations with treasurers from middle-market corporates who are looking to work closer with their banking partners, more so than ever before. “In this Basel III world, there is a real risk that banks may not have as keen an appetite to work with some clients,” he says. “Treasurers of these companies want to be proactive in managing the relationship by having a continuous dialogue to ensure the bank will continue to provide them with banking facilities.”

The need to have honest communication with banks is a point also noted by AT&T’s Rogers. “I think a good bank will understand that if they can’t deliver on a specific requirement, the corporate will have to go elsewhere for this, as long as this is correctly communicated.” It works both ways, and Rogers highlights that it is only by telling the bank what you need that they will they be able to ensure they deliver.

Aside from simply talking to your banks, there are other steps that corporate treasury teams can take to maintain a healthy relationship. For EY’s Kennedy, nothing is more effective than a bank rationalisation project. “This sends a clear message of intent to remaining banking partners that there will be a larger wallet to share across a smaller number of relationship banks, on the basis that the bank continues to deliver exceptional service and products to the client.”

Other treasury teams have employed more innovative methods. American multinational, Brocade, for instance, suffered from a poor, unstructured management process with its banking partners that delivered less than adequate results for the treasury department. The company therefore initiated an innovative scorecard project that would allow them to better evaluate their banking partners and improve the relationships (see Brocade case study).

Microsoft is another company that has looked at this area closely after finding out that it met with over 40 banks on a regular basis just for debt capital markets and share buyback work. This equated to four months a year in bank meetings, roughly a third of their working hours. To work out the return on investment (ROI) of all this work, Microsoft have built a solution that enables them to track their bank relationships by recording the time spent working with them and the outcome of these meetings. The bank relationship tracker has delivered many benefits including ensuring that their banking group develop value-add ideas and solutions for the team.

Case study

Kerry Group – The RFP as a relationships tool

While some treasurers may simply see the RFP as a functional tool that allows the treasury to understand its different options and make an informed decision when implementing a new solution, Trevor Horan, Treasurer, Global Cash & Liquidity at Kerry Group, believes it can be more than this – and, in fact, that it can be an effective relationship management tool.

For Horan, the key to achieving this is to make the RFP process open and transparent. The openness derives from ensuring that the tendering process is open to all banks (something which some may argue is ill-advised given the additional workload this creates for the treasury). For Horan, this is misguided. “I believe that all banks the company has a strong relationship with should be offered the opportunity to win the business. By doing so, we demonstrate that we value their support and the relationship we have. We are also not limiting our options.”

Of course, like all treasurers, Horan does not want to have to sift through endless RFPs. So instead of not inviting banks to take part in the RFP process, Horan has built in a mechanism that reduces the amount of responses the treasury gets to its RFP. “At the start of the RFP document, just after the index, we include a list of key criteria that has to be matched,” he says. “If this criteria cannot be matched then we suggest that the rest of the document is not completed. This is where being transparent about the process prevents the banks from wasting time filling out the document and also reduces our workload when it comes to analysing the responses.”

We also make sure that those involved in the tendering process know who else has been invited, who has made the shortlist and who we are moving the process forward with,” he adds. “By doing this there are no secrets between us and our key counterparties, something that is appreciated by all involved.”

After the RFP process has been carried out each respondent is also given the opportunity of a full de-brief of their proposed solution in due course. “The feedback from banks to this de-brief has been extremely positive, it helps them understand why their solution was not selected and maintains strong relationships, something that is very important to Kerry Group,” says Horan.

Ebbs and flows

Whilst these strategies may provide corporates with the tools to manage banking relationships as they stand today, there are many changes that continue to happen in the industry. Even some of the most prominent bankers are claiming that the industry will shapeshift and look very different in the years to come. And these are changes that may profoundly impact the relationships corporates have with their banks.

It is technology, and more specifically the rise of fintech, that will pose the biggest threat to banks. Indeed, we have already seen fintech companies picking off the profitable areas of the banks business in the retail space – is the commercial space next?

Anthony Eldridge, Financial Services Leader at PwC Singapore, certainly thinks that this could be a real possibility. “The question is not can technology companies replace banks, it is, do they want to? These companies are very happy to be picking off the profitable areas of financial services but once you become a fully-fledged bank you step into a quagmire of regulation and compliance.”

There may need to be a change in approach, to ensure banks maintain their position. “Banks are often asking the question ‘what can fintech do for us?” says Eldridge. “But I am increasingly of the belief that banks need to be asking what can we do for the fintechs.” In his view, the landscape is changing so quickly and these firms are developing highly sophisticated technology so readily that a situation could exist where banks end up as simply a utility service behind fintech, providing compliance and risk management.

This is certainly an interesting picture being painted, but do corporates also believe this could happen? Views seemed to be mixed. Dovey, for instance, foresees big changes coming. “I do see banks being disintermediated by technology firms in the future,” she says. “Companies like PayPal make it so easy for our customers to make a payment that they force you as a corporate to take that payment method seriously – you don’t have any choice. If a fintech company can win the hearts and minds of the general customer, they are everyone’s customer. Corporates will have to follow.”

AT&T’s Rogers is less convinced, but highlights that there is a need for banks to move quickly to avoid being cut out. “I think the banks realise they have to develop and move quickly to offer products for the future; they need to talk to corporates to understand needs and how the future may change and what requirements are needed,” she says. Again it is the regulatory environment that may create difficulties for banks in this endeavour.

Either way, it seems certain that we are set for more changes in the financial services industry to take place over the coming years and it will continue to be imperative for the treasury department to stay abreast of these to ensure that the company has a banking group that is fit for purpose. For now, clear and honest communication, both ways, will be key to ensuring that this happens.

The KYC challenge

Recent events have shown that regulators are becoming increasingly serious about KYC. And this is having a detrimental impact on corporates and their banking relationships.

Compliance is a concern for banks, with know your customers (KYC) and anti-money laundering (AML) rules for example requiring constant attention. This is having a knock on effect on their corporate customers.

The growing burden was highlighted in a recent global study conducted by Thomson Reuters, who polled 822 decision makers around KYC related matters. The headline finding: 89% of those corporates surveyed have not had a good KYC experience in recent years.

Perhaps unsurprisingly, it is those corporates with multiple banking relationships who are feeling the most KYC-related strain. The main reason for this being the lack of standards. As a result, banks are asking for differing documents based on their own interpretations of the regulation.

Whilst it is quite understandable that banks are being highly cautious around KYC – as we have seen it is costly to fall foul of the regulators. What is less understandable, from a corporate perspective at least, is that the burden is being added to by the banks own internal shortcomings. To highlight this point, 40% of respondents said that they had to deal with many different people within an individual bank and 34% said they were asked for different documents by different people within that bank.

The result of this being that corporates are spending more time than ever on KYC-related activities, with 63% of respondents saying this has increased over the previous 12 months. 21% of these said it has increased significantly.

Bad experiences

So what does this all equate to in real terms for Christopher Emslie, Singapore Treasurer and his team at ABB? “As a large corporate with multiple banking relationships we spend a large amount of time on KYC, especially when there are changes to our organisations or our banking relationships,” he says.

The worst experience for ABB was an account opening process that took a staggering nine months (34 days is the typical average time at present). “The issues were on delays from all sides,” he explains. “This biggest was a change in regulations in the banks presiding country which were not communicated effectively.

“A few years ago, I could probably have countered this poor experience with some examples of better ones, but these are very few and far between, even though some banks really do go out of their way to be accommodating they are still bound by their internal rules and things beyond their control.”

Despite the best efforts by the banks, corporates are beginning to vote with their feet when they encounter overly complex and burdensome KYC requirements. “In some instances it is easier to walk away than to try and overcome some of the issues, this is not good business practice but in some instances it is just impossible to comply,” explains Emslie.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.