As the global economy finds its feet, corporate treasurers continue to push for efficiencies in their operations. Meanwhile, financial institutions and endusers of financial services are working through a deluge of regulatory changes. The rationale for collaboration between banks and clients to overcome these hurdles and create a sustainable growth environment for all is more compelling than ever.

Mark Tweedie

EMEA Head of Corporate and Public Sector Sales, Treasury and Trade Solutions

Mark Tweedie has been with Citi for over 14 years and is the Europe, Middle East and Africa (EMEA) Head of Corporate and Public Sector Sales, for Treasury and Trade Solutions (TTS). EMEA is the largest region for TTS with a presence in over 50 markets. Tweedie is responsible for addressing the cash management, working capital, treasury and trade service /financing needs of clients across all sectors, through the mobilisation of the Citi infrastructure, resources and TTS solution set.

From Basel III to payments reform, the financial world is undergoing substantial change. While the need for a more stable regulatory environment that addresses the shortcomings of the pre-crisis years is undisputed, the impact of these changes on both corporates and banks is significant. Well-intentioned regulation is in many ways making it more difficult and more expensive to do business, and is threatening the ability of companies to leverage growth opportunities. Illustratively the new credit conversion factors in Basel III have been raised markedly forcing banks to keep more risk capital for Export Agency Financed transactions and Letters of Credit, in turn making such instruments more expensive for the end-client. Moreover the cost of compliance (relative to revenue) for smaller banks has gone from 5% in 2009 to 7% in 2013, with larger banks seeing their compliance cost: revenue ratio going from 1% to 2% in the same period.

The question, then, is how can corporates and banks work together to lessen the burden of the new regulatory order? How can collaboration create a stable future for transaction banking, thereby safeguarding companies’ financial and commercial flows? In a world of increasing digitisation and globalisation (heightened cross-border mobility of capital, labour and goods), national ring-fencing of balance-sheets and financial transaction taxes create inherent policy and practices conflicts.

Regulatory impact

Over the last five years, financial reform has been driven by two aims: achieving financial stability and improving consumer protection, standards and harmonisation. Under the ‘financial stability’ banner, the main measures include Basel III, bank recovery and resolution planning; whereas the latter covers everything from the Single Euro Payments Area (SEPA) to the European Market Infrastructure Regulation (EMIR). The result is both opportunity (treasury transformation to maximise standardisation under SEPA XML with greater availing of payment on behalf of account and operating models) and threat, in the form of funding access and increased cost, with banks facing higher risk capital limits and Return on Risk Capital requirements.

Under Basel III, banks must rightly shore up their balance sheets, whilst certain reforms are decreasing attractiveness and thus returns on short-term cash. Trade finance is increasingly concentrating with the global leaders who have proven “supplier onboarding” pedigree and large asset distribution capacity.

While at first glance the outlook may seem bleak, positives are emerging from this change, says Mark Tweedie, Head of Sales EMEA, Treasury and Trade Solutions, Corporate and Public Sectors at Citi. “Basel III may be altering the availability of lending, but it’s also improving the quality, transparency and dialogue of lending decisions. It is critical that both borrower and lender are clear on what factors make the facility attractive. All parties realise that balance sheets have finite capacity and that returns are driven by ancillary flow and episodic business awards,” he explains.

“Banks and their corporate clients are being brought closer together through open discussion around the need for reciprocal relationships. Indeed, discussions between banks and their clients are going deeper than ever before and looking more at the genuine needs of each client’s business. Banks are now strategic partners, working ever more closely with the corporates to whom they lend, with wide relevance across multiple constituencies in the client office eg for full-service transaction banks; finance, treasury, procurement, sales finance, credit control, Shared Services, marketing, travel and business development.”

Basel III is prompting treasurers to keep a closer eye on their bank facilities ie revisiting the size of unused credit facilities and diversifying beyond overdrafts and general purpose loans, in order to avail of finely priced/shorter tenor working capital assets. “Corporates and banks are sitting together to determine the most appropriate way to fund operations, which can only be a positive step. At Citi we are collaborating with our clients’ treasury and tax teams to map legal entities, asset and cash flow exchanges, in order to better refine cash management and foreign exchange solutions,” says Tweedie.

A stable future for all

This dialogue creates a more sustainable and meaningful business relationship for both parties. The business world recognises that transaction banks grease the wheels of global commerce. “It is our job to support complex client ecosystems by managing clearing, settlement and liquidity, therein enabling global buyers and sellers to facilitate international trade,” Tweedie notes.

“We provide liquidity through the supply chains of companies – upstream and downstream – and ultimately facilitate the free movement of cash which is the lifeblood of the global economy,” he adds. “Our aim is to provide a low-cost, highly efficient environment which allows businesses and society to prosper. There is a great deal of mutual benefit in what we as transaction banks, and our clients, are trying to achieve.”

In fact, says Tweedie, “corporate banking which encompasses transaction services, is at the core of the ‘socially useful’ banking concept, which has been the subject of much debate since the global financial crisis.” To illustrate this point, he cites two examples of Citi’s engagement in society.

The first is the bank’s work with Italy’s Istituto Nazionale per la Previdenza Sociale (INPS), the primary Italian government pension fund. INPS has 410,000 pensioners in 131 countries and is one of the largest pension funds in Europe in terms of overall pensions paid. The fund’s management team wanted to improve efficiency and control over these payments.

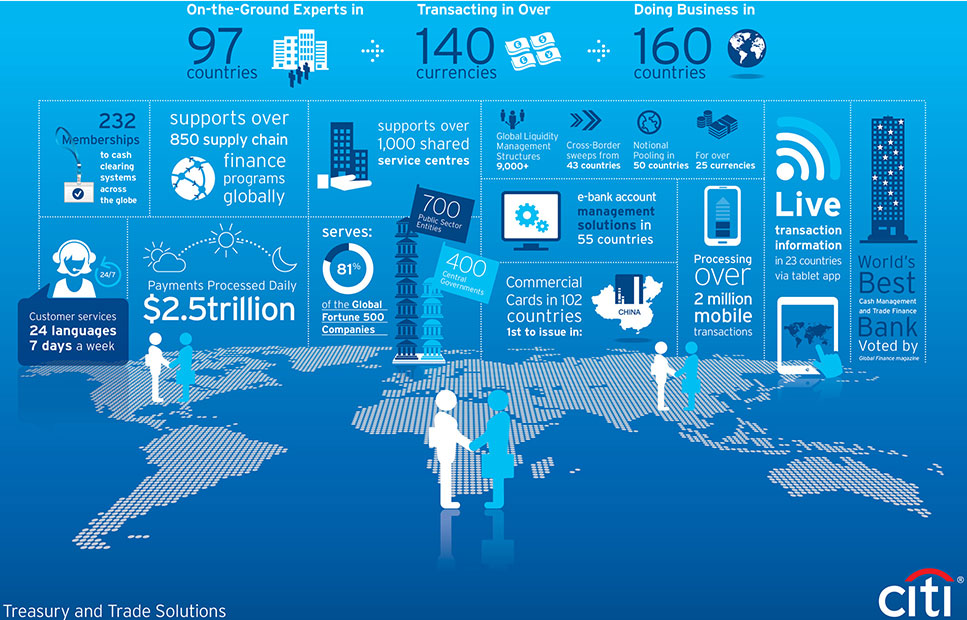

Diagram 1: Citi Treasury and Trade Solutions

“Governments have recognised that a number of their citizens relocate post-retirement to pastures new. We are working with the Italian pension fund, as we are with a number of governments, to provide adjacent services that help them to better manage their cross-border payment flows to expats,” he outlines. “We provide a complete payment service suite to INPS, based on Citi’s WorldLink global payment platform, along with value-added services including Proof of Life certification, central pensioner database management and an interactive website and call centre for INPS’ pensioners.

“In other words, we are enhancing the service provision and going beyond mere payment settlement business. Just look at the Proof of Life example – to prevent payments going out to deceased individuals, we issue annual forms for certification and manage the approval process to ensure that payments are only made to active beneficiaries. This saves the Italian state the time and inconvenience of having to recall the funds. Against a backdrop of ongoing fiscal austerity, we certainly see this as a socially useful service.”

The second example Tweedie refers to takes us from Italy to Africa, where Citi is working with almost 200 development sector organisations. “The Non-Governmental Organisations (NGOs) in Africa are looking for more efficient ways to ensure that foreign aid and investment is being used effectively. They want to be satisfied that the donor flows are both tracked and monitored in terms of effectiveness,” he explains. In a banking context, this means increasing visibility, which creates greater accountability; and shifting from paper to electronic instruments, leading to increased control. “We are seeing the same needs in the Corporate space where illustratively in Nigeria we are assisting the airlines move from an instance of online booking with offline (physical) cash settlement, to an integrated model leveraging the new digital Faster Payments instant settlement system.”

Citi already has experience of doing this in other developing economies and is therefore well-placed to do so across Africa.

Case study

ACF and Citi join forces to support flood victims

Action Against Hunger|ACF International (ACF) is a global humanitarian organisation committed to providing communities with access to safe water and nutrition. The organisation runs life-saving programmes in around 40 countries benefiting five million people each year.

In 2011, tropical storm Washi swept through the Philippines, bringing flooding and rainfall that killed more than 900 people. As part of its emergency intervention programme for the families affected by the storm, ACF needed to disburse funds within one month to more than 2,000 victims on behalf of a major donor. The funds were to be used exclusively to purchase food items from a specific retailer in order to ensure that donations were channelled towards alleviating hunger and preventing misappropriation of funds.

A customised Citi Prepaid Card programme, based on a closed-loop system, ensured that cards could be used only at the designated grocery store. In order to comply with the Philippines Central Bank’s Know Your Customer requirements, Citi and ACF developed a simple process whereby photographs of beneficiaries were used for identification.

The cards provided essential support to vulnerable families. While compliance with KYC rules can be frustrating, particularly in the absence of government issued identity cards, the solution suggested by Citi was convenient and could be implemented quickly, whilst complying with the relevant regulations.

Improving infrastructure

Elsewhere, Tweedie says that Citi is seeing more and more global RFPs from clients wanting to understand how developments such as common monetary zones are leading to borderless banking. “Companies are looking to explore opportunities for rationalisation of bank accounts with global systemically important banks that have footprints across the key growth markets and a mantra of technological innovation and solution delivery.”

Citi has invested across Africa and was proud to be a lead sponsor of the March EuroFinance Africa, London Event. “We have also invested heavily in helping national banking bodies, and customers within the local markets to make the most of new technology and evolving payment methods.”

Citi acted in an advisory capacity around the Nigerian central bank’s move to a real-time gross settlement system (RTGS). And in Kenya, Citi has enabled both B2C and B2B mobile payments through advocating mPesa. According to Tweedie, “Banks such as Citi are helping the developing economies to leverage technologies for processes improvement, while enabling them to leapfrog the legacy steps and constraints that many developed markets are still struggling with.”

A catalyst for change

The same rationale around seizing the opportunities that change brings – whether regulatory or innovation-driven – also applies to Citi’s work with corporates across the globe. “Right now, we are helping clients to use SEPA as a catalyst for change,” says Tweedie. “By educating clients on the wider benefits of SEPA, we are able to help them to streamline their euro bank account structures, improve their reconciliation rates, maximise DPO through payment warehousing, and improve their supplier’s experience via beneficiary advising.

At the same time, since SEPA uses the XML format, which is an industry standard, we are working with clients towards the adoption of a common interface. This will not only allow for vastly streamlined bank-to-corporate connectivity, but at a time of immense regulatory and political reform, will assist in lowering the cost of doing business.”

In addition to working towards standardisation of messaging formats, Tweedie believes that transaction banks have a responsibility to streamline and standardise client documentation, making it far more intuitive. This statement of intent is certainly being put into action at Citi. “In EMEA, on the back of our clients’ feedback, we have consciously and systematically reduced our local account conditions by 50%. We are also working to automate and digitise as many paper processes as possible. Working with our technology partners and our innovation labs we have created a common document taxonomy and internal search capacity to reduce duplicative client document requests. These changes will save time and money, while improving tracking and monitoring for everyone.”

“To that end, Citi is also introducing additional value-added services for clients, such as online audit certifications. “Clients need to provide certified statements at the end of the financial year and we have recognised a need for specialisation in that area. As such, we have a Direct Debit styled self-service site which provides audit confirmations. In the EMEA region this process only applies to Western Europe.”

This, says Tweedie, is all part of the bank’s increasing focus on self-service technologies. Such an approach minimises the need for contact with bank support staff and empowers clients to help themselves. “A lot of the queries we receive are around payment confirmations and statements and we are working very hard to equip clients with the answers to those queries via our technology. It is quicker, more efficient, more direct and leads to an improved client experience.”

Upgrades have been made to the Citi Direct e-banking platform. “Citi has upgraded the platform to enhance its functionality and improve its self-service elements. Rather than forcing clients to migrate with all the associated disruption, upgrades are less invasive but show clients rich new features in a controlled fashion. We recognise that clients have challenges interfacing with large banking institutions such as ourselves and we are committed to delivering the highest level of customer experience, so this is a key priority for us.”

“It is partially as a result of the regulatory environment, redefining rules and operating frameworks, that more candid and in-depth discussions have been taking place between banks and their clients. And as a result of these increasingly transparent relationships, corporates are providing more detailed and honest feedback to their banks around their end-to-end propositions. So, by driving collaboration, regulation is ultimately contributing to a better transaction banking experience. We know we have much work ahead but there is an institutional conviction to delighting our clients.”

Citi Treasury and Trade Solutions (TTS)

Citi Treasury and Trade Solutions (TTS) offers the industry’s most comprehensive range of digitally and mobile enabled treasury, trade and liquidity management solutions, platforms, tools and analytics. TTS continues to lead the way in delivering innovative and tailored solutions to its multinational corporation, financial institution and public sector organization clients. Based on the foundation of the industry’s largest proprietary network, with banking licenses in over 100 countries and globally integrated technology platforms, TTS’ deep local market knowledge, expertise and insights assist clients to meet their business objectives.