Even through the inflationary pressure of the pandemic and war in Ukraine has eased, longer-term structural factors will keep inflation high.

The pandemic and war in Ukraine accomplished what central banks were unable to for decades: end too low inflation. Covid greatly reduced labour supply (due to illness, caring for others and fear of working) while governments maintained demand with massive support measures. Demand also shifted sharply from services to goods, creating all sorts of bottlenecks. This gave companies more pricing power (which they used) and gave commodity prices a lift which was then amplified by the war between two major commodity producers, Russia and Ukraine.

The pandemic and the Ukraine war resulted in two major shocks to the world economy that led to higher inflation. This should also mean that when the effect of these shocks wears off, inflation will quickly fall again and return to pre-corona crisis levels. Inflation has started to fall in Europe and the US and the decline is likely to continue.

Base effects, as prices are compared with those already high prices of last year, the year-on-year change comes out lower.

Economic growth has weakened and lower growth is on the horizon as the stimulative effect of waning supply side problems fades and spending of hoarded savings stops. Moreover, much of the negative effect of previous interest rate hikes has yet to be felt in the economic data. Lower growth reduces the pricing power of firms and will also cool the labour market, reducing upward pressure on wage growth.

As a result, the inflationary effect of the corona crisis seems to be gradually dissipating. Furthermore, the Ukraine war may continue, but its effect on commodity prices has diminished significantly.

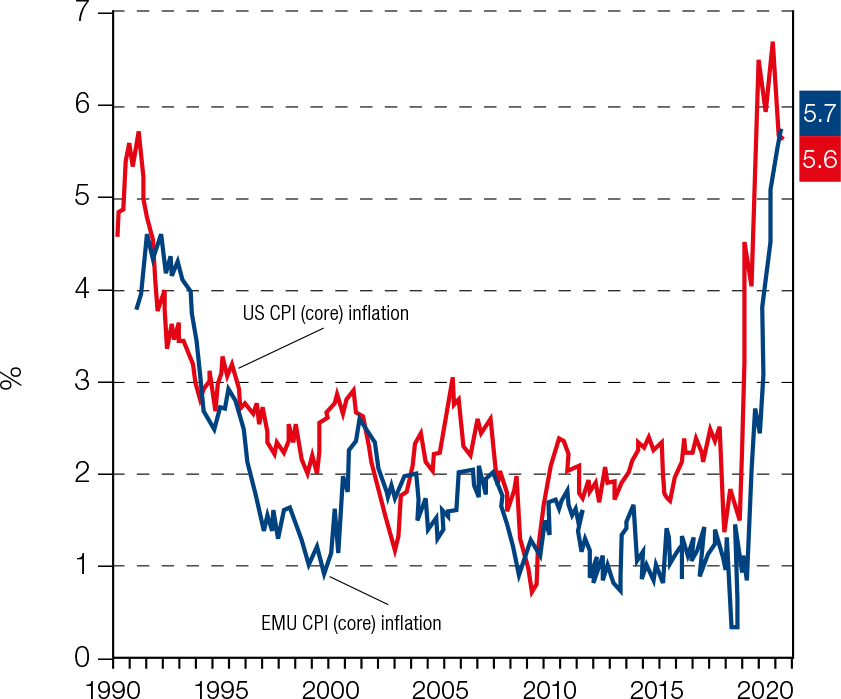

Chart 1: From deflationary threat in the past decades to inflationary fears in the recent years

Source: Refinitiv Datastream/ECR Research

Return to old normal unlikely

However, there are a number of reasons why we strongly doubt that inflation will actually return to pre-corona crisis levels and stay there. Besides corona and the war, there are a number of other developments contributing to the current high inflation rate:

In many countries, the labour force is on the cusp of shrinking (China and some European countries) or has already shrunk, like in Japan. This increases labour market tightness and reduces international wage competition, giving workers more bargaining power. Ageing also means that the demand for healthcare personnel increases; a sector that has low productivity growth compared to other sectors.

The cumulative effect of very loose monetary policy since the credit crisis. During this period, much more money was created than could be absorbed by the real economy. The excess money has mainly flowed into asset markets, where it has led to asset-price inflation. This has created a huge reservoir of inflationary potential just waiting for a trigger to break the dam.

This trigger came in the form of higher government deficits. Through issuing more government bonds and distributing the proceeds to businesses and consumers, suddenly much more liquidity flowed into the real economy and combined with less supply led to consumer-price inflation.

Due to the transition to renewable energy and under pressure from ESG considerations, less capital has been available in recent years to invest in oil and gas extraction and commodity production in general. Meanwhile, the demand for commodities remains high for the time being, if only to enable the transition to renewable energy (and the associated infrastructure). This will accelerate the situation of insufficient supply of commodities and will thus cause rising commodity prices.

Without these developments, it would be highly doubtful that the pandemic and war alone would have led to inflation rising so quickly – and hanging around. Rising commodity prices as a result of the war would otherwise have greatly inhibited growth (and thus overall inflation), and without the large amounts of excess liquidity, much higher government deficits would have quickly led to higher interest rates. This would have crowded out businesses and consumers, who therefore would not have been able to borrow or only borrow at prohibitive high interest rates. Wider fiscal policy would then have mainly led to a shift in demand (from the private sector to the public sector), while higher interest rates would have caused substantial downward pressure on asset prices.

It is therefore too short-sighted to base inflation expectations on the impact of the Ukraine war or how quickly the effect of the corona crisis (and the hefty fiscal stimulus during that period) wears off. We do see this having a major impact on headline inflation in the coming months to quarters, but we see core inflation falling much less sharply due to the other factors. For the coming years, we expect these and other factors mentioned above to structurally create more upward pressure on inflation.

Long-term implications for asset prices

This year’s (expected) decline of inflation will not be a harbinger of a return to the pre-pandemic days which central banks conducted expansionary monetary policies to get inflation to rise towards 2%. In fact, over the next few years we expect the five developments mentioned above to put more structural upward pressure on inflation. We expect the markets to gradually start discounting this in the coming quarters. Furthermore, we think that some of these factors (continued loose fiscal policy and tight labour markets due to ageing) will cause core inflation to fall less sharply than headline inflation ahead.

There are a number of consequences for financial markets:

Long-term interest rates, based on weakening growth expectations and declines in (headline) inflation, may fall further this year. However, this fall will be limited and followed by a rise to new highs in the coming years.

Real interest rates will likely turn positive, as bond investors will increasingly take into account that central banks will do too little to really control inflation and would rather accept higher inflation than risk a credit crunch.

In principle, stocks would benefit from a further decline in long-term interest rates and the expectation that central banks will accept higher-than-target inflation to avoid a deep recession. But in our view, this positive effect will be offset in the coming years by increases in long-term real interest rates and low growth prospects due to ageing populations and a higher share of low-productivity sectors (defense and healthcare) in total GDP. In addition, we expect governments to more heavily tax corporate profits to foot the bills of the increasingly expensive welfare state.

Over the coming years, we expect the prices of inflation-linked bonds and real assets (gold, commodities and infrastructure) to rise due to inflation and expectations that central banks will accelerate monetary devaluation.