China’s domestic bond market is in a new phase of its rapid evolution, as the investor base is broadening and strengthening with increased interest from institutional buyers focused on the front end of the market. The attraction for these typically more-conservative investors is a large and liquid market, which caters to a wide range of very secure borrowers, and offers more attractive yields than those available on bank deposits. However, a key idiosyncrasy of China’s market at this stage of its development is heightened volatility at the front end of the yield curve, with considerable implications for risk and returns. Understanding the nature and drivers of volatility is important for navigating China’s markets, in our view, and active management can help turn this challenge to investors’ advantage.

China’s domestic bond market is in a new phase of its rapid evolution, as the investor base is broadening and strengthening with increased interest from institutional buyers focused on the front end of the market. The attraction for these typically more-conservative investors is a large and liquid market, which caters to a wide range of very secure borrowers, and offers more attractive yields than those available on bank deposits. However, a key idiosyncrasy of China’s market at this stage of its development is heightened volatility at the front end of the yield curve, with considerable implications for risk and returns. Understanding the nature and drivers of volatility is important for navigating China’s markets, in our view, and active management can help turn this challenge to investors’ advantage.

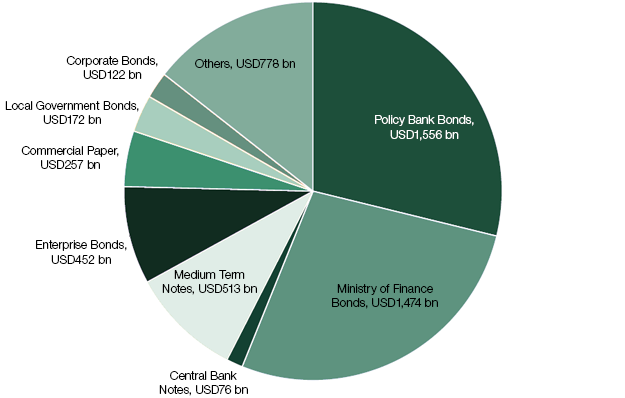

China’s ascendance in the ranks of global markets has been swift. In the past couple of decades, China’s bond market has grown in both size and depth to become the third largest in the world at more than $4 trillion, according to the Bank for International Settlements, with trading volumes topping $43 trillion in 2013. This liquidity has become a key attraction for institutional investors globally. Most corporate treasuries have already gained exposure to Chinese fixed income via money market fund (MMF) investments, and pension funds and sovereign investors are showing increased interest.

Figure 1: Size and Composition of China’s Domestic Bond Market

Source: China Bond, as of July 2014

The benefits of market access via MMFs include exposure to the highest quality issuers in the government-, quasi government- and banking sectors, potentially higher yields than are available on bank deposits and, depending on the fund, management consistent with global standards for triple-A rated stable net asset value (NAV) funds such as tight limitations on interest rate risk. Moreover, we believe active management is necessary to help address anomalies in China’s short-term markets that have significant implications for investor portfolios.

Most corporate treasuries have already gained exposure to Chinese fixed income via money market fund (MMF) investments, and pension funds and sovereign investors are showing increased interest.

Not Your Average Market – Nature and Drivers of Volatility

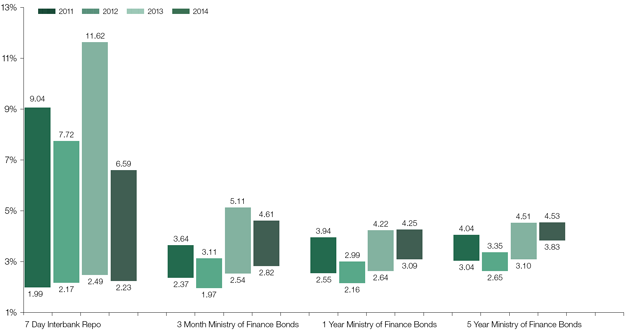

For institutional investors, the most significant anomaly in China’s rates markets is their volatility. The typical relationship between tenor and range is inverted, so that instead of increasing with the length of maturity, volatility is most pronounced at the front end of the yield curve. Figure 2 shows that the annual ranges of yields on shorter-dated securities are considerably wider than those for longer-dated securities. This phenomenon has been consistent over a number of years, though year-to-date the range is substantially smaller than it was in 2013, when a midyear credit crunch drew international attention. In this instance, short-term benchmark rates rose several percentage points on the convergence of several catalysts for volatility: seasonal effects, foreign exchange flows, reduced bank lending and a pullback in support from the central bank.

Figure 2: Annual Ranges in Yield for Select Instruments

Source: Wind, as of July 2014

Given the degree of potential volatility in China’s markets, it pays to understand the drivers. The most predictable one is seasonal, as liquidity constraints are common around major holidays such as Chinese New Year and key quarter-end balance dates. Around holidays, the fluctuations are attributable to consumption patterns and resulting bank behavior. For example, consumers draw down savings for vacation spending, and immigrant workers returning to their home provinces bring cash for their families. To cater to this demand, banks accumulate cash by borrowing in the repurchase (repo) markets and offering higher yields on interbank deposits. The quarter- and year-end spikes are also common but less pronounced, and they occur when banks store up cash to meet required loan-to-deposit ratios at the end of each reporting period.

The typical relationship between tenor and range is inverted, so that instead of increasing with the length of maturity, volatility is most pronounced at the front end of the yield curve.

These seasonal effects are closely followed by the central bank, which has the capacity to intervene via its open market operations to alleviate liquidity pressures. That said, market observers note that the People’s Bank of China (PBoC) has been known to tolerate significant levels of volatility before intervening materially, as was the case in May/June 2013. Moreover, the triggers for intervention are not fully transparent, and no clear pattern of intervention has emerged.

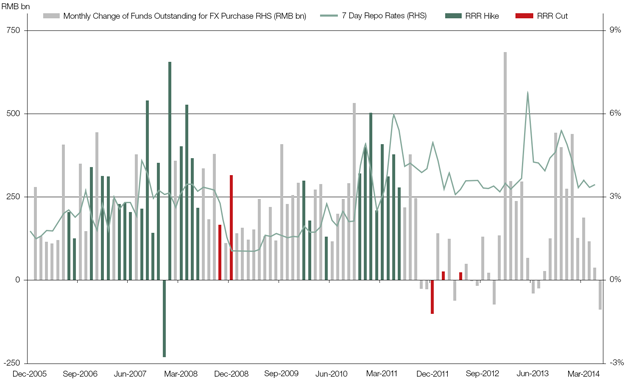

Volatility in China’s short term markets is also partly attributable to fluctuations in foreign capital flows. Over much of the past decade China has seen strong inflows as international investors have looked to capitalize on the Renminbi’s appreciation versus the US dollar. These flows, all else equal, inject liquidity into China’s financial system, exerting downward pressure on money market rates. In order to stabilize money market rates, the PBoC has historically relied on the reserve requirement ratio (RRR), which determines the share of deposits banks must set aside in case of financial trouble. By raising this ratio periodically, the PBoC created extra demand for liquidity from banks, which helped absorb foreign currency inflows. As Figure 3 shows, between 2005 and 2011 when inflows were generally substantially positive, the RRR was consistently raised (with the exception of reductions during the global financial crisis). However the RRR is a blunt tool: rates would head lower as foreign currency inflows accumulated, then spike after each RRR hike.

Over much of the past decade China has seen strong inflows as international investors have looked to capitalize on the Renminbi’s appreciation versus the US dollar. These flows, all else equal, inject liquidity into China’s financial system, exerting downward pressure on money market rates.

Since 2011, foreign currency flows have become more volatile and two-way in nature, in part due to slowing growth outcomes and most recently due to the PBoC doubling the currency’s daily trading earlier this year. At the same time, the PBoC has implemented new tools, relying increasingly on Open Market Operations of varying tenors to help fine-tune market liquidity. However, as noted above, the triggers and patterns of its interventions are unpredictable.

Figure 3: Forex Flows, Repo Rates and Periods of RRR Adjustment

Source: Wind, as of July 2014

Case for Active Management

In China particularly, such insights are not just helpful to understand market behavior – they are instrumental in helping manage interest rate risk. Active management of an asset portfolio’s duration can aid in reducing adverse market movements when rates are rising, and allow increased yield generation when yields are falling. Volatility of this kind raises important risk and return considerations for investors in short-duration or money market funds as interest rate fluctuations increase the potential for higher earnings, but also the risk of underperformance on adverse market moves.

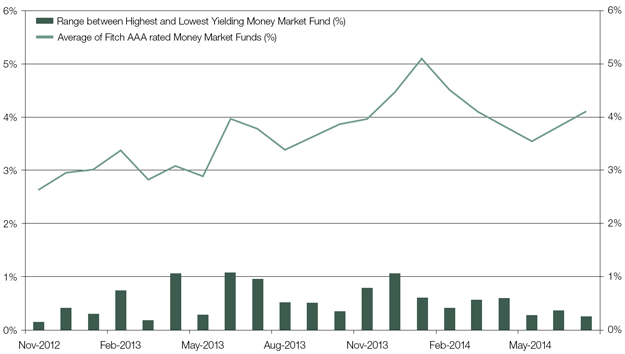

The volatile front end provides substantial scope for individual specialists to differentiate their performance, as managers better able to anticipate and position flexibly for large movements in short rates are likely to be able to deliver better returns for clients. Figure 4 highlights this point by showing a significant distribution of performance across a range of Fitch AAA money market strategies. Though all are limited to a 75-day weighted average maturity (WAM), the return differential between the highest and lowest yielding funds can often exceed 50bps.

Fig 4: Fitch AAA-rated RMB Money Market Funds/Collective Investment Schemes: Average Monthly Yield and Range1

Source: Wind, as of July 2014 1RMB Fitch-AAA funds launched after November 2012 are not included in this investment universe.

In sum, we see a trend of continued expansion in the investor base for Chinese debt, and particularly with the increased attention from more conservative institutional buyers. For these investors, the attractions of risk diversification in a liquid market of increasingly high quality are clear. However, alongside these benefits are factors idiosyncratic to this stage of China’s market development, which contribute to volatility. As a result, an informed approach is key to navigating China’s markets, in our view, and investors need to take an active role in managing the risks to reap the rewards.

For more information on Goldman Sachs Global Liquidity Management, please contact:

This material is provided for educational purposes only and should not be construed as investment advice or an offer or solicitation to buy or sell securities.

THIS MATERIAL DOES NOT CONSTITUTE AN OFFER OR SOLICITATION IN ANY JURISDICTION WHERE OR TO ANY PERSON TO WHOM IT WOULD BE UNAUTHORIZED OR UNLAWFUL TO DO SO.

Prospective investors should inform themselves as to any applicable legal requirements and taxation and exchange control regulations in the countries of their citizenship, residence or domicile which might be relevant.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice. This material is not financial research and was not prepared by Goldman Sachs Global Investment Research (GIR). It was not prepared in compliance with applicable provisions of law designed to promote the independence of financial analysis and is not subject to a prohibition on trading following the distribution of financial research. The views and opinions expressed may differ from those of GIR or other departments or divisions of Goldman Sachs and its affiliates. Investors are urged to consult with their financial advisors before buying or selling any securities. This information may not be current and GSAM has no obligation to provide any updates..

The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur.

Views and opinions expressed are for informational purposes only and do not constitute a recommendation by GSAM to buy, sell, or hold any security. Views and opinions are current as of the date of this presentation and may be subject to change, they should not be construed as investment advice.

Although certain information has been obtained from sources believed to be reliable, we do not guarantee its accuracy, completeness or fairness. We have relied upon and assumed without independent verification, the accuracy and completeness of all information available from public sources.

The website links provided are for your convenience only and are not an endorsement or recommendation by GSAM of any of these websites or the products or services offered. GSAM is not responsible for the accuracy and validity of the content of these websites.

United Kingdom and European Economic Area (EEA): In the United Kingdom, this material is a financial promotion and has been approved by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom by the Financial Conduct Authority.

Asia Pacific: Please note that neither Goldman Sachs Asset Management International nor any other entities involved in the Goldman Sachs Asset Management (GSAM) business maintain any licenses, authorizations or registrations in Asia (other than Japan), except that it conducts businesses (subject to applicable local regulations) in and from the following jurisdictions: Hong Kong, Singapore, Malaysia, and India. This material has been issued for use in or from Hong Kong by Goldman Sachs (Asia) L.L.C, in or from Singapore by Goldman Sachs (Singapore) Pte. (Company Number:198602165W), in or from Malaysia by Goldman Sachs(Malaysia) Sdn Berhad (880767W) and in or from India by Goldman Sachs Asset Management (India) Private Limited (GSAM India).

Australia: This material is distributed in Australia and New Zealand by Goldman Sachs Asset Management Australia Pty Ltd ABN 41 006 099 681, AFSL 228948 (’GSAMA’) and is intended for viewing only by wholesale clients in Australia for the purposes of section 761G of the Corporations Act 2001 (Cth) and to clients who either fall within any or all of the categories of investors set out in section 3(2) or sub-section 5(2CC) of the Securities Act 1978 (NZ) and fall within the definition of a wholesale client for the purposes of the Financial Service Providers (Registration and Dispute Resolution) Act 2008 (FSPA) and the Financial Advisers Act 2008 (FAA) of New Zealand. GSAMA is not a registered financial service provider under the FSPA. GSAMA does not have a place of business in New Zealand. In New Zealand, this document, and any access to it, is intended only for a person who has first satisfied GSAMA that the person falls within the definition of a wholesale client for the purposes of both the FSPA and the FAA. This document is intended for viewing only by the intended recipient. This document may not be reproduced or distributed to any person in whole or in part without the prior written consent of GSAMA. This information discusses general market activity, industry or sector trends, or other broad based economic, market or political conditions and should not be construed as research or investment advice. The material provided herein is for informational purposes only. This presentation does not constitute an offer or solicitation to any person in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it would be unlawful to make such offer or solicitation.

Canada: This material has been communicated in Canada by Goldman Sachs Asset Management, L.P. (GSAM LP). GSAM LP is registered as a portfolio manager under securities legislation in certain provinces of Canada, as a non-resident commodity trading manager under the commodity futures legislation of Ontario and as a portfolio manager under the derivatives legislation of Quebec. In other provinces, GSAM LP conducts its activities under exemptions from the adviser registration requirements. In certain provinces, GSAM LP is not registered to provide investment advisory or portfolio management services in respect of exchange-traded futures or options contracts and is not offering to provide such investment advisory or portfolio management services in such provinces by delivery of this material.

Japan: This material has been issued or approved in Japan for the use of professional investors defined in Article 2 paragraph (31) of the Financial Instruments and Exchange Law by Goldman Sachs Asset Management Co., Ltd.

Confidentiality

No part of this material may, without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any form, by any means, or (ii) distributed to any person that is not an employee, officer, director, or authorized agent of the recipient.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.