Offering the possibility of streamlined cash management processes, improved working capital efficiency and increased visibility and control over corporate spend, corporate cards are the treasurer’s new best friend. In this Product Profile, we look at the ways in which a tailored card programme can assist treasurers through the tough economic times. We also look at market developments and best practices.

Finding better and more efficient ways to manage the company’s cash, improve liquidity and make working capital ‘sweat’ are imperatives for today’s treasurer. The ongoing economic turmoil has made access to credit more difficult and led companies to look internally for cost savings and operational efficiencies that will assist in ensuring the company’s cash flow remains at a viable and sustainable level.

Andy Lyons

“Implementing and optimising a commercial cards programme is an excellent way to do this,” says Andy Lyons, Commercial Card Sales at Lloyds Banking Group. “Although many companies are familiar with corporate charge cards for managing their business travel and expenses, the card market – and its benefits – go far deeper than that. Purchasing cards, for example, are now coming into focus as a means of moving companies out of a labour-intensive paper environment, towards a streamlined, end-to-end procure-to-pay process.” When it typically costs between £25-30 to process an invoice manually, the benefits seem obvious.

Although many companies are familiar with corporate charge cards for managing their business travel and expenses, the card market – and its benefits – go far deeper than that.

But cards are about more than ‘quick-win’ cost savings. “Card programmes, whether they revolve around corporate cards, purchasing cards, prepaid cards or an amalgam of those, are a very effective means of helping clients to manage both internal and external workflows more efficiently,” continues Lyons. “Yes, there are significant cost savings to be made, and naturally that is a driver, but there a number of additional benefits to consider. While these may take slightly longer to materialise, or may be more difficult to tangibly measure, it’s a question of extending value across areas of the business that often haven’t previously been touched.”

So, how do commercial card programmes fit into the broader cash management cycle and how can they assist corporates in weathering tough economic times?

Adding value through cards

Looking to implement or to optimise an existing card programme may, understandably, be just another project on the ‘to do’ pile for treasurers at the moment. Taking a more macro view however, a number of the challenges that are currently being faced by treasury, procurement and finance departments can be overcome through the deployment of a suitable card programme.

Take for example the need to deliver improved cash management and working capital efficiencies. Using a corporate credit card scheme, companies can effectively eliminate the need for advance cash flow, whilst giving their employees an easy-to-use payment method that is widely accepted, wherever they may be travelling.

Using a corporate credit card scheme, companies can effectively eliminate the need for advance cash flow, whilst giving their employees an easy-to-use payment method that is widely accepted, wherever they may be travelling.

Corporate cards also enable procure-to-pay processes to be streamlined. For instance, the manual processing of reimbursements for an employee’s expenses incurred on their personal card can be enhanced with the integration of transaction data into an expenses or accounting software package. In addition, companies increasingly want their employees to use corporate cards because of the valuable management information (MI) that can be gained and analysed through online technology.

This financial data enables the Accounts Payable (AP) department to have increased visibility and control over expenditure, and therefore greater insight into the company’s overall cash position. “A corporate card implementation is a swift, cost-effective means of tracking and controlling the business-related expenses of employees. By removing paper out of the system and having data available at the click of a button, corporates can find out what has been purchased, where, when and by whom, as well as whether it is in line with their governance policies,” comments Lyons. This helps to ensure that company money is spent with preferred suppliers, and that all negotiated pricing deals are being taken advantage of.

It is not just corporate credit cards that deliver these benefits. Purchasing cards, also known as p-cards, which have long been used for low-value purchases in the corporate space are being used to bring greater visibility and control over tail-end business spend. Detailed, level three line item data which includes purchase information such as a description of the product, quantity and price is made available and similarly this information can be used to see exactly what is spent and where improvements can be made. The real savings opportunity available does not only come from the tail-end spend though, but through convincing corporates to use their cards to procure their more strategic supplier spend.

“Budget expenditure can also be managed in a far more granular way as corporates can add specific “codes” to the data that they have gleaned, assigning purchases to the appropriate cost centre and general ledgers for example,” continues Lyons. “Where cash is king for the traditional payments market, MI is king for cards.”

How quickly clients obtain that MI is also key. Corporates no longer want to wait to receive statements on a monthly basis, they want the relevant information available throughout the month, rather than having a shock at the end of the four weeks. Card programmes can deliver this and banks can add additional value with reporting functionalities, as well as seamless integration into the company’s internal systems for automatic reconciliation, controlling and efficiently managing budget allocation as well as overall spend analysis.

Corporates no longer want to wait to receive statements on a monthly basis, they want the relevant information available throughout the month, rather than having a shock at the end of the four weeks.

Elsewhere, spend information can be useful in consolidating purchases – and indeed currencies. As such, rather than making a number of one-off payments to a particular supplier, a single monthly payment can be processed. Not only does this further streamline operational processes, it also offers the opportunity to extend the company’s payables cycle. For instance, when paying by cheque, the float is usually only a few days. By using a card solution the supplier can be paid a few days after the purchase, but the company does not have to pay off the amount on the card until it becomes due – potentially adding an extra twenty-eight days or so to the monthly payables cycle.

By using a corporate credit card, the supplier can be paid a few days after the purchase, but the company does not have to pay off the amount on the card until it becomes due – potentially adding an extra twenty-eight days or so to the monthly payables cycle.

Reaching further

Where external workflows and relationships are concerned, card programmes also have a lot to offer. An area of particular benefit is that of buyer-supplier relationships. Through the use of a flexible card programme, both buyers and suppliers can meet their often conflicting needs more readily. In other words, suppliers get paid on time and in a more consistent manner. This helps the supplier’s cash flow, meaning that they are less likely to encounter financial troubles and are also more likely to look favourably on the buyer, thereby improving relationships and potentially leading to discounts for loyalty. Looking after suppliers in this way also helps treasurers to align themselves with industry best practice.

According to Lyons, “This should provide sufficient ammunition for buyers to talk again with their suppliers about how the benefits of using cards can significantly outweigh the merchant costs that the supplier has to bear. Moreover, the supplier will see improved internal efficiencies themselves – for example they would not have to take on the risk of accepting cheques, or the labour-intensive task of chasing late payments.”

But this discussion touches on one of the most difficult challenges associated with card acceptance in the corporate space today: perception. “It’s relatively easy to identify the opportunities that a card programme could bring,” admits Lyons. “The hardest part of the process is to convert people across the organisation from working in a paper-based environment to an electronic one. For instance, a number of companies feel comfortable working with cheques – as this is what they know – but really a prepaid card or a p-card could make the process much easier for everyone: from procurement to finance and operations.”

There is also a tendency to feel that by taking away the tangible elements of a process (ie paper), a corporate is relinquishing its control over that process. “Paper is seen as safe. There is nervousness around cards, in particular in areas such as fraud. In actual fact, card fraud is less frequent than fraudulent cheques. It’s about getting people comfortable and helping them to understand where commercial savings and operational efficiencies can be made.”

The more corporate spend that a company can put onto a card as part of a common process, the more they will benefit.

When corporates are open minded about their end-to-end procure-to-pay process, is where banks such as Lloyds can really add significant value, says Lyons. “Clients often have a preconceived idea about what cards can deliver for them and when this is the case, they don’t tend to derive the maximum amount of benefit. So what we want to be able to do is pass on intellectual capital and experience to our clients. Rather than seeing them realise 10% of their commercial savings through cards, we want them to get up to the 75-80% mark. The more corporate spend that a company can put onto a card as part of a common process, the more they will benefit.”

A dynamic market

Despite a reduction in the amount of corporate travel and business expenditure being sanctioned, the commercial card market continues to blossom.

Solid growth is expected over the coming years, and with that we are starting to see exciting developments in card offerings.

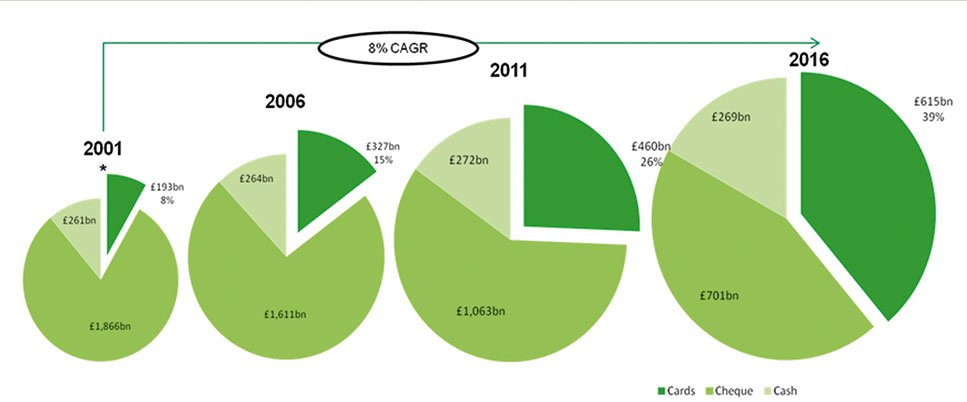

Diagram 1: Cards’ value as a proportion of total UK payments – 2001-2016

* Total value includes inter-bank, inter-branch and in-house items, but excludes cash acquisitions

Source: Payments Council, 2010

will see the launch of five new card products from Lloyds Bank, which will complement the bank’s existing corporate card and p-card solutions. Elsewhere, an interesting market development that Lyons sees is growth in the commercial cards space as the usage of cheques declines.

Indeed, although cheques have now been given a reprieve from being abolished in the UK, cards are beginning to take a large chunk of market share. Figures from 2001 show that cards represented a mere 8% of UK payments, in 2011 that figure was 26%.

By 2016, 39% of UK payments are expected to be made by card. “I believe prepaid cards will soon become a very popular alternative to cheques among corporates,” explains Lyons. In his view, it really isn’t a question of ‘if’, but ‘when’.

Implementation is just the start

For those corporates contemplating the implementation of a card scheme, or putting their existing programmes out to tender, Lyons has some parting words of advice: “Really look end-to-end in the procure-to-pay process, spend time analysing what different expenditure you have and be honest about how much control you genuinely have over that expenditure today.

Also, how long after the event do you know that something has been purchased? In answering these questions, the benefits of a well-run card programme – and where your current set-up is falling down – should become clear.”

However, continues Lyons, “A card programme is not just about the implementation and on-boarding, it is about the ongoing management and development of that programme. At Lloyds, we work closely with treasurers, procurement and finance teams to really help them understand the processes that should be put in place to achieve this optimisation – such as how best to manage the movement and exportation of spend data into their accounting software or TMS.”

In summary, by leveraging technology and the expertise of bank (and in-house) card gurus, companies can achieve compelling results across the business through commercial cards usage.

Case study

Lowcostholidays.com

Salman Rasool

Group Finance Director

Lowcostholidays.com has realised significant operational improvements, resulting in a 200% increase in card transactions processing over the last 12 months. The Lloyds Card team has really worked hard to ensure that there are no service failures and the reporting capabilities, via their sophisticated management information portal, is tailored to allow quick and efficient reconciliation. This is absolutely essential in a high volume transaction based business such as Lowcostholidays.com and the solution Lloyds delivers meets this goal in full.

We receive excellent support from the Lloyds Programme Development team who are always available when we need them for our day-to-day business needs, as well as proactively demonstrating their thought leadership in bringing new ideas to us.

We receive excellent support from the Lloyds Programme Development team who are always available when we need them for our day-to-day business needs, as well as proactively demonstrating their thought leadership in bringing new ideas to us. The customer support they provide on a programme and cardholder level is extremely impressive.

Lloyds always deliver and we would highly recommend them – they are a true partner to our business.

Lloyds Bank

Lloyds Bank delivers corporate banking and risk management solutions to businesses with over £15m annual turnover. We have a network of relationship teams across the UK, as well as internationally, with the mix of local understanding and global expertise necessary to provide long-term support and advice to our customers.

We offer a broad range of sophisticated financing solutions, spanning structured and asset finance, import and export trade finance, securitisation facilities, and risk management. Our product specialists provide bespoke financial services and solutions including tailored cash management, supply chain financing, international trade and debt capital markets funding.

Contact details:

Andy Lyons

Head of Card Sales, Transaction Banking

Red Lion Court

Southwark

London

SE1 9EQ

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.