With mounting pressure to improve controls and efficiency and to free up trapped cash, the treasurer’s role continues to expand. How then can group treasury optimise internal processes and the use of company cash when the treasury centre is lean, budgets are constrained and there are only so many hours in a day? In this Business Briefing we discuss the current issues facing group treasurers and explore approaches that can be taken to resolve these.

Changing requirements

In an evolving market landscape, treasurers need to capture and formalise best practices for their organisations in order to address new complexities and challenges. Corporations have been moving steadily toward working capital optimisation by automating treasury functions through an integrated and co-ordinated approach. Automation also allows treasury to focus on its strategic and analytical functions by minimising time spent on routine operational processes.

The challenge, however, is to be able to relate recognised treasury best practice to the needs of the organisation, and in such a way that the business is not locked into rigid arrangements which restrict the company’s responsiveness and competitive edge. General trends such as globalisation, increased control and improved internal efficiency are influencing the areas on which corporate treasurers are currently focusing. These areas include:

Visibility of cash.

Group treasury needs to know how much cash the organisation has around the world, where that cash is, and how treasury can make use of it. Achieving visibility in this area can ensure that cash truly is a corporate asset, meaning that it is accessible and can be used to decrease short-term borrowings.

Compliance.

With the advent of SOX and increasingly strict audit requirements, the tools that treasurers use are coming under close scrutiny. It is no longer sufficient to run spreadsheets as pseudo treasury systems. Best practice requires an integrated, multi-functional treasury system which also incorporates relevant treasury policies.

Risk management.

Dealing with various entities in different locations increases FX risk, operational risk and counterparty risk. With many companies no longer having a regional treasury centre structure, it is the group treasurer who needs analytical tools to address and monitor emerging company and subsidiary risks efficiently.

Flexibility.

Treasury should have the flexibility to diverge from its historic policy where appropriate, not only to avoid potential losses but also to take advantage of opportunities presented by market or industry developments.

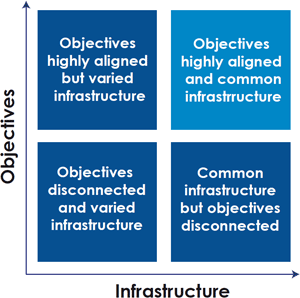

The theory behind these objectives is all well and good, but putting theory into practice is often a different matter. A major hurdle faced by group treasury in implementing new practices or improving existing systems is the disconnection between the subsidiaries and the group treasury centre, which often stems from a misalignment of infrastructure and objectives (see below).

Challenges in group treasury

There are two sides to the issue of disconnection.

Firstly, there is often insufficient information flow with regard to what the subsidiary company is doing, for example in terms of their currency positions, or simply how they are managing their cash forecasts and the standards that they apply. This in turn generates control concerns.

Secondly, there may be a mismatch between group treasury’s needs and the priorities of the subsidiary. Group treasury seeks to manage risk on an aggregated, long-term basis. Subsidiaries, in contrast, have more immediate needs, such as funding requirements. As such, operating companies often resort to hoarding cash to cover any unexpected cash outflows, or to be able to respond to customers’ and suppliers’ needs.

How then can group treasury address this disconnection effectively?

Information management: real-time

The information reported to group treasury is typically not useful to the subsidiary itself and it is, therefore, often seen by the subsidiary as a secondary priority. The reporting process can be labour intensive and there is an element of duplication in reporting both locally and centrally for cash and risk management purposes. A group-wide information management tool may enable the treasury to automate tasks such as cash flow forecasting for the subsidiaries. If the tool also delivers real-time information, this will help the subsidiaries to understand the immediate impact that their reporting has on the company as a whole.

Hedging

An improved flow of information gives more opportunity to identify, measure, evaluate and ultimately to hedge FX risk, whether at subsidiary or group level and whether internally or externally. Running a centralised system that will monitor these hedges and the hedge exposure will not only reduce the workload but also ensure that all processes are fully auditable and compliant. Linking company-wide FX exposure will also bring treasury closer to the business.

Creating discipline

One approach which may be used to align the subsidiaries with the group treasury is to bring discipline to inter-company settlement processes. This can either be done centrally or by giving the subsidiaries a tool which makes it easier for them to be managed. For example, a tool which allows inter-company netting of payables and receivables will further reduce the number of external transactions, thereby reducing cost and counterparty risk and benefitting all business units.

Getting buy-in

Unless there is a culture where the corporate centre demands and the subsidiary responds, any proposition made to the subsidiaries needs to be a value-add for them too. Group treasury should market itself to the subsidiaries and gather support by taking into account different practices and cultures. There is also a need to recognise that a discipline suitable for one line of business may not be appropriate for another, due to being in different markets or varying stages of development. The challenge is ensuring that the subsidiaries realise that all disciplines need to roll up into group treasury in a consistent and efficient way.

Overcoming the obstacles

Large corporates that have well staffed treasury departments and sophisticated technologies have managed to solve the majority of these challenges, but not without a budget commensurate with their size. Most treasury departments do not have the budget for a large technology spend however, so what is the answer?

In an ideal world, operating a single ERP system group-wide and having only one global bank and one set of policies would go some way to solving the disconnection issues that group treasury faces. In reality, however, most corporates do not have a single set of systems, standards and relationships, with some companies not even having their payables and receivables in the same accounting system. Group treasury departments need tools that will combine real-time cash position reporting and forecasting together with straight through processing (STP) and current, detailed information to help them overcome these problems.

Traditional solutions

Historically, corporates have had two options available to them: either they buy a standalone treasury management system (TMS) or they buy a treasury module for their ERP system. Both approaches have their benefits and downsides:

Advantages

They are widely available, proven solutions.

A TMS has sophisticated treasury specific functions.

A TMS can be hosted by a systems provider, which gives more flexibility for upgrades.

ERP treasury modules can offer increased visibility as ERPs are company-wide systems.

An ERP offers opportunities for standardisation.

The potential for comprehensive front, middle and back-office reporting.

Disadvantages

The cost of implementation is high.

The time dedicated to a TMS or ERP implementation can be years, not months.

A TMS is standalone and can be difficult to integrate with existing systems.

ERPs are managed centrally, which means that upgrades have to be made according to a central schedule – this can be slow.

ERP systems are not always designed specifically to interface with external parties.

Many companies run several ERP systems – which would mean that buying a single treasury module would be much like deploying a standalone TMS.

Interview

J.P. Morgan’s Treasury OnLine application

Seamus Desouza

Treasury Services

What is J.P. Morgan’s Treasury OnLine application?

Treasury OnLine (ToL) is an all-in-one application that enables risk analysis, dealing, cash flow forecasting and inter-company netting for corporate treasury centres. It electronically links subsidiaries to the head office and automates manual processes in line with treasury policy. It’s a browser application and nothing needs to be installed at the client’s location.

The structure is ‘modular’, but these are not modules in the classic bolt-on TMS or ERP sense. There’s a dealing module, a risk analysis module, a cash module and a netting module all integrated to use a common database.

Could you explain a bit more about how the modules work?

Really it’s all down to how the client allocates permissions to the users, the functions they seek and how those functions are set up. If we take netting, for example, does the client want multiple netting centres? Should the netting cycles overlap? How will items settle – net or gross? We can also consider netting by payables, receivables or both and inter-company or third-party netting. So you can see that it’s very flexible.

Clients can execute basic FX deals such as spots, forwards and swaps in the dealing module, both inter-company and externally. Again, these can be restricted by entity and by individual user, in terms of which of those instruments they can use. Clients can set limits so that if subsidiaries trade above a certain limit, the deal is flagged for central approval but the subsidiary can continue to use the system whilst awaiting approval.

With the risk analysis module, clients can load their balance sheet straight up out of the general ledger or they can load up balance sheets at subsidiary levels and roll them up into consolidated view to see their currency exposures. The client can also load up multi-currency revenue and expense to determine earnings-at-risk, and also identify subsidiary cash flows that may be used as earnings-at-risk hedge proxies.

In the cash module, bank account information can be consolidated with daily, weekly and monthly forecasts to improve multicurrency liquidity management. Currency exposure can be analysed and hedging proposals can be generated in line with pre-defined policy parameters.

Who is the target customer and how will they benefit from choosing ToL?

ToL will be most useful to mid-size to large corporates with a multinational footprint and, typically, with a very lean treasury staff just in the corporate centre, not distributed around the world. It is less likely to offer the same level of value to the very largest corporates because they have typically invested in a single ERP or a TMS or both and they have all these disciplines.

ToL will give group treasurers a basis for more efficient cash management and risk management process because a lot of the emails, spreadsheets and routine data manipulation can be eliminated. It can be more effective because both treasury and the operating companies are working on real-time information. ToL is a scalable solution which can provide 90% of the benefits of a TMS at a fraction of the cost and implementation time. The corporate decides how complex it needs its operational environment to be and this can be rapidly parameterised into series of permissions to meet those needs.

Industry innovation

Although there are tools available that are not full-blown TMSs, such as multi-lateral netting products or cash management products, these applications do not usually combine both of these disciplines together with risk management and dealing capabilities. J.P. Morgan’s Treasury OnLine (ToL) is an example of a solution from a leading bank which combines all of these capabilities together with global access to J.P. Morgan’s latest market research in one holistic, web-based solution.

In addition, J.P. Morgan is currently implementing a new platform for its proven ToL application so that it now has enhanced functionality, allowing the client to integrate its treasury policy into its daily functions. The application is designed to facilitate medium to large sized corporates to eliminate some of the issues faced by their group treasuries with only a modest effort and budget. ToL is designed to allow information to flow freely from subsidiary companies to the group treasury so that group treasury can have increased visibility over the company as a whole and integrate cash management into business processes.

ToL is a multi-bank application that runs off an integrated single database for execution and reporting. The application provides advance knowledge and timing of cash flows. It can also monitor the currency of cash flows. Data extracted from the corporate’s ERP, AP (Accounts Payable) or AR (Accounts Receivable) systems is aggregated by currency, out into the future, and can then be enriched by remote input of current information from the subsidiaries’ locations. ToL also incorporates FX instruments which are aimed at managing uncertainty of timing and amount, often a significant challenge for group treasurers.

ToL Dashboard

With ToL, treasury is positioned in the middle of the revenue and expenditure cycles where treasury manages currency risk and working capital efficiency while subsidiaries can focus on being responsive to their customers’ needs and supplier obligations.

Where is the smart money?

The current environment demands the deployment of risk management tools and techniques that strike a balance between operational flexibility and strong financial discipline – flexibility to respond to business opportunities and discipline to protect cash as a corporate asset. Such tools will need to be globally available, but with the ability to deploy by business or region and to address each discipline, such as cash forecasting, inter-company netting and currency exposure management.

If a company has specific and highly sophisticated hedging needs, these will probably be best met by a full scale TMS, which will of course require sufficient resources and planning. If, however, a corporate is looking to benefit from the type of solutions which a TMS can provide, but on a scalable level, and without the implementation time and cost, an all-in-one treasury application that allows multi-bank, cross-border transactions could be an ideal solution. Corporates will be able to benefit from browser based tools and carry out all the functions they would expect from an off-the-shelf software house package, including real-time updates.

One final challenge is presenting a convincing business case for treasury’s proposed technology spend. However, if, as Desouza says, 90% of the benefits that the largest corporations have gleaned from having sophisticated technology in place can be obtained through a relatively modest effort, the advantages of this type of approach are clear.

J.P. Morgan Treasury Services

With more than 50,000 clients and a presence in 36 countries, the Treasury Services business of J.P. Morgan is a top-ranked, full-service provider of innovative payment, collection, liquidity and investment management, trade finance, commercial card and information solutions to corporations, financial services institutions, middle market companies, small businesses, governments and municipalities worldwide.

With increased global trade, clients face a growing need to manage worldwide exposures while automating payment processes, driving internal efficiencies and maintaining robust compliance and control mechanisms. J.P. Morgan helps clients handle the complexities and challenges of the evolving cross-border payment landscape, providing benefits such as:

Cost savings with rationalised account structures and competitive FX rates.

Convenient and flexible local currency accounts.

Operational efficiency through access to electronic payments in the form of cross-border funds transfers, global ACH, and draft capabilities.

A high rate of straight through processing through advanced technology.

Advanced features such as workflow solutions and risk, hedging and exposure management.

J.P. Morgan Treasury Services is the world’s largest provider of treasury management services and a division of JPMorgan Chase Bank, N.A., member FDIC. More information can be found at www.jpmorgan.com/ts

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.