In the autumn of 2008, the banks at the heart of the Western financial system suffered a severe crisis, the likes of which had not been seen since the Great Depression. Governments around the world attempted to co-ordinate their efforts in introducing regulatory changes aimed at building a more stable, less leveraged global banking system.

Today, with banks having to scale back their risk taking activities in response to Basel III, attention is switching to the so-called shadow banking sector. In 2010, the G20 leaders gathered at the Seoul summit voiced their concerns about the role of shadow banking in the financial crisis and the Financial Stability Board (FSB) was asked to work with other international regulatory bodies in developing recommendations to strengthen oversight of the sector.

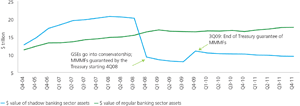

The functions performed by organisations outside of traditional banking – and, crucially, outside of the scope of banking regulation – have become increasingly important to the day-to-day operation of the global financial system over the course of the past decade. The Deloitte Shadow Banking Index published last year estimates that on the eve of the financial crisis, the total assets under management in the shadow banking system stood at over $20 trillion dollars, eclipsing even that of the traditional banking sector.

Since then, regulatory pressures have brought about a decline in the sector – in absolute terms and relative to the traditional banking sector. By 4Q11, assets were estimated at $9.53 trillion, more than 50% lower than at the 2008 peak (see Chart 1).

Chart 1: Shadow banking versus traditional banking sector assets (US), 2004-2011

Source: SIFMA, Federal Reserve Bank of New York, Federal Reserve Flow of Funds, Haver Analytics and Data Explorers

Despite this recent decline, introduction of the regulatory proposals currently being discussed will undoubtedly have a profound impact on the global economy. The credit intermediation, liquidity and maturity functions provided by shadow banking institutions are essential to many corporates. Consequently, there is concern in the market that an overly stringent approach to regulation may damage the ability of non-banks to provide services upon which a large number of businesses still rely.

Blinded by the light

These concerns are particularly acute when it comes to the reform of the money market fund (MMF) industry. Tighter oversight of the industry has been on the agenda ever since the financial crisis, when the exposure to Lehman Brothers debt securities caused the Reserve Primary Fund to lower its share price below $1 and ‘break the buck’. Other funds in the US and Europe were underwritten by their national governments. In the wake of those events, the Securities and Exchange Commission (SEC), who regulates financial markets in the US, adopted revisions to rule 2a7, requiring funds to improve liquidity and the credit quality of their portfolios.

“SME treasurers are probably using CNAV MMFs because they are straightforward, easy to book and report on a tax basis. Now, if the market changes to a new way of doing things which requires you to change your accounting processes, then you may just think it is not worth the hassle and return to bank deposits.”

Aymeric Poizot, Head of EMEA Asset Manager Ratings team, Fitch

However, further reform of the industry is almost certain. One proposal, considered by the SEC and other international regulatory bodies such as the European Commission (EC), is to introduce a mandatory conversion to variable net asset value (VNAV). The backlash against constant NAV (CNAV) funds is based on the perception that investors will ‘run’ from a CNAV fund more readily as they aim to ensure they receive their full $1 per share value before the fund value fall below one and ‘breaks the buck’. However this theory was not borne out by the behaviour witnessed in the crisis. Indeed many who did redeem shares from prime CNAV MMF promptly reinvested in government funds – which are also operated as CNAV.

But some opponents of this approach argue that a mandatory conversion to VNAV poses a serious threat to the MMF industry. A recent study found that of the investors surveyed, only 16% use VNAV funds alone. Meanwhile, a clear majority, 25% – equating to 50% of those who use MMFs – are said to prefer CNAV funds. Aymeric Poizot, Head of Fitch’s EMEA Asset Manager Ratings team, says the survey revealed two commonly cited reasons for this apparent preference. Firstly, there is the inherent simplicity of the tax and accounting treatment required for users of CNAV funds; not every business will have the resources to cope with the added complexity a move to VNAV will bring, he asserts.

“If you are a treasurer for a small or medium-sized enterprise (SME), then this might cause a headache,” he says. “They are probably using CNAV MMFs because they are straightforward, easy to book and report on a tax basis. Now, if the market changes to a new way of doing things which requires you to change your accounting processes, then you may think it is not worth the hassle and return to bank deposits.”

Secondly, Poizot argues that a switch to VNAV may complicate risk management for corporates – something rather paradoxical, considering the overriding objective of the proposal is to reduce the level of risk in the market. “This is something the regulators do not appear to be fully aware of,” he begins, explaining that when a treasurer uses a CNAV fund they are using a product with a very clear risk profile – the fund is rated by multiple agencies and has very strong governance. “But if all funds were to switch to VNAV, then there is a strong argument to be made that the risk profile of the industry would be less clearly defined.”

If it’s not broke…

Susan Hindle Barone, Secretary General of the Institutional Money Market Fund Association (IMMFA), is more cautious on the potential impact of a compulsory move to a floating NAV. “A lot of investors would be seriously inconvenienced if funds were forced to become VNAV. They really appreciate the simplicity of using a CNAV fund and the last thing we want to do is discourage them from achieving diversification in their cash holdings by pushing more of their money back into bank deposits,” she says. However, if regulators persist and all the funds had to convert to floating NAVs, she believes that, given time and a pragmatic approach in tax and accounting treatment, many investors would transfer over to VNAV MMFs. The trouble is, she says, the premise that CNAV funds are inherently more risky is something the industry simply does not agree with.

“VNAV does not tackle the fundamental reason why investors will redeem from an MMF, namely that they are concerned about the credit quality of a particular security in that fund.”

Joanna Cound, Head of Government Affairs and Public Policy, Europe at BlackRock

This argument is reinforced by a recent research paper published by the Columbia University School of Law, which studied the comparative run rate of the two types of MMF during what is now known colloquially as “Lehman week”. The study found no empirical evidence to suggest that CNAV funds have a higher risk of “breaking the buck” in times of market stress. On the contrary, the two factors observed to contribute to run risk for MMFs were higher yields (indicating additional risk) and the perceived capacity of sponsors to support the fund.

It is the futility of the VNAV approach in terms of enhancing the stability of MMFs that concerns Hindle Barone most. “What worries us is that by switching the funds from CNAV to VNAV the regulators believe that with this they will be making a great contribution to global stability – a great step forward – yet we think that it will achieve nothing. It won’t remove risk or interconnectedness from the market, and that is what really alarms us.”

It is an argument echoed by Joanna Cound, Head of Government Affairs and Public Policy, Europe at BlackRock. Blackrock stresses that it is not opposed to either a conversion from CNAV to VNAV or to capital in principle but, like IMMFA, BlackRock does not believe the floating NAV proposal will be effective in addressing client redemptions in the event of a crisis. “It does not tackle the fundamental reason why investors will redeem from MMF, namely that they are concerned about the credit quality of a particular security in that fund. Clients ran during the 2007/2008 financial crisis because they didn’t know which funds might be invested in Lehman Brothers or any other name in the headlines at that time. It was clearly a run to safety.”

A similar argument is also made against capital buffers, another proposal currently being weighed up by European regulators. Having some capital put aside for times of market stress may make MMFs marginally more stable and better able to withstand idiosyncratic risk. “But such a level of capital will not be sufficient to protect a MMF facing mass client redemptions in the midst of a systemic crisis,” according to Cound. “The amount of capital required to achieve this would be so large that it would make MMFs uneconomic for any fund manager to offer to their clients.”

The alternatives

Both IMMFA and BlackRock are at pains to emphasise that they are not against regulation of MMFs per se; it is just that they do not agree on the efficacy of the above proposals. An alternative approach, one which the industry would almost certainly back, would be to introduce prescribed liquidity buffers. Unlike mandatory VNAV and capital buffers, a liquidity requirement would go right to the heart of the problem. When markets become stressed, as they did in 2008, the most effective protection for a fund is to have natural liquidity in its portfolio so that it can meet client redemptions without having to sell assets at low prices in a distressed market.

Another idea, currently being promoted by Blackrock, is to require fund managers to introduce redemption gates and liquidity fees which are activated when certain triggers are met. When the market enters a period of stress, an objective trigger is hit and the Board or Management Company would be obliged to gate the fund and reopen the next day with a liquidity fee. Clients who needed their cash would have access to it – providing they pay a small fee to ensure equal treatment of all the investors in a fund – but the overall volume of client redemptions would be reduced. “It would be the most effective means of mitigating a run on MMFs,” Cound says. “Unlike mandatory conversation to VNAV and high levels of capital, which limit choice for investors, liquidity fees preserve the benefits of CNAV for those clients that require such MMFs, whilst effectively addressing the concerns of regulators.”

End times for MMFs?

The regulators will certainly be aware of the concerns many in the MMF industry have over the current direction of reform. Yet a proposal drafted by the EC appears to indicate that the regulators are intent on pressing ahead, regardless of the opposition. The draft, which was leaked to the Financial Times in April, gives funds a choice of two options – either convert to a floating NAV or retain a 3% capital buffer.

If these proposals are introduced without amendments, corporate investors who maintain large cash balances in MMFs may well begin looking at the alternatives. For operational funds which require overnight liquidity, a return to bank deposits, even in the current ultra-low interest rate environment, seems to be the only feasible solution. But many companies are currently also holding onto funds as part of a longer-term cash reserve. For these funds, a short-term bond exchange traded fund (ETF) – such as the PIMCO Enhanced Short Maturity ETF – may be an option for consideration.

“There will be a solution,” says Hindle Barone. “Like any equilibrium, it will find the right level. All we hope is that this is not to the detriment of investors because after all that’s who the products are for.”

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.