It may seem like a rather simple task, especially in the day and age of internet banking, but in practice, achieving full visibility across a group’s cash position is often harder than it looks. And although some of you will be reading this, happy in the knowledge that you know how much cash you have and where it is, many treasurers will not.

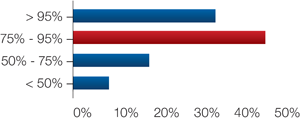

For proof of this, just look at the results of Ernst & Young’s April 2012 study entitled ‘Reflecting on the future: a study of global corporate treasuries’. Approximately a third of treasury departments have daily visibility of more than 95% of the cash in the company, whereas just under half of respondents claim to have sight of 75% to 95% of the company’s cash on a daily basis. Somewhat shockingly, nearly 10% of respondents have less than 50% visibility.

Chart 1: Percentage of company wide cash visible to treasury on a daily basis

Source: Ernst & Young’s, ‘Reflecting on the future: a study of global corporate treasuries, April 2012

Failure to achieve sufficient visibility over the company’s cash carries significant risk. In fact, without clear visibility, companies cannot adequately control group cash. In turn, this means they cannot use that cash at optimum efficiency, or maximise investment opportunities for it. Reducing borrowing costs and improving foreign exchange risk management will also be extremely challenging without full visibility and control.

“It is hardly surprising, therefore, that the majority of companies (69%) plan to further improve visibility of and control over cash,” says the survey. The question, then, is how best to go about this?

Overcoming visibility hurdles

The level of cash visibility that a company can achieve will be heavily influenced by the level of centralisation, with centralised treasuries naturally having an advantage over their decentralised counterparts. In fact, centralisation is one of the key organisational tools that companies use to improve visibility.

Elsewhere, the company’s size and sector can affect visibility levels, as can the rate of growth of the business and its geographical footprint. Nevertheless, there are some fundamental considerations that all companies can take into account when identifying major challenges to visibility – and investigating how these can be overcome.

Technology

This is the obvious answer to most visibility challenges. In fact, visibility is largely an exercise in deriving cash positions by accessing up-to-date bank account balances – the art is how to make that as simple (and automated) as possible. “We just download the information we need from the relevant online banking systems. The majority of the work is done automatically, with some small amount of manual input,” says Stephen Webster, Group Treasurer, QinetiQ. “As a FTSE 250 company, we don’t have a particularly complex set-up or extensive international presence, so with the ability to access our entire bank balances online, we really don’t find visibility to be a problem.”

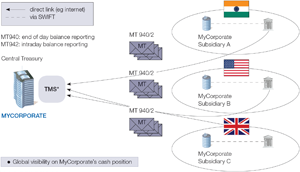

Many very large corporates, or those with decentralised operations, often do not find this quite so easy – with extended bank networks and myriad reporting solutions in use. This is where SWIFT comes into its own. “It’s a great way to standardise reporting and get daily visibility over your global cash positions,” says Julia Persson, Former Deputy Head of Treasury at A.P. Moeller Maersk. Similarly, Edward Mundt, Senior Treasury Manager at Asurion, believes that “with SWIFT reporting, any treasury management system (TMS) can give you visibility into the vast majority of your global cash.” The diagram on the next page illustrates how this could work.

Many of the world’s biggest corporates report vastly improved visibility through the use of SWIFT. In fact, Microsoft, which has in the region of 200 subsidiary businesses, 110 global bank partners and over 1,000 bank accounts, has reportedly achieved 99% visibility over global cash through the use of SWIFT’s MT (FIN syntax) and MX (XML syntax) messaging standards.

Nevertheless, this solution isn’t foolproof. “Not all banks use SWIFT to the full extent,” warns Maciej Müldner, CFO, Skanska Romania. “This is one of the reasons that companies can find Eastern Europe a challenge from a visibility point of view. Take Romania, for example, with such low demand for SWIFT from corporates in the country, the value proposition simply isn’t there for many of the local banks to support it.” Certain Asian countries, such as Korea, pose similar challenges. “Even if you can get hold of an MT940 from the bank, expect it to be significantly more expensive than you are accustomed to in the US or Europe,” says Asurion’s Mundt. “Also, don’t anticipate that it will necessarily be in English.”

Diagram 1: End of day and intraday balance reporting

*Treasury management system

Source: SWIFT

Bank relationships

Let’s be clear, this is not an invitation to go and have it out with your bank about your visibility issues; however, your choice of banking partner(s) will inevitably have an impact on the level of visibility that you are able to achieve.

Lenovo, for example, has implemented a single bank model that allows the company to achieve superior levels of visibility. “We have domiciled all our operational accounts with a single bank,” says Damian Glendinning, Treasurer of the computer manufacturing giant. “This solution may not be to everyone’s taste, but it means that all the data is immediately available in the internet banking system of the bank in question, and can be downloaded easily into spreadsheets, or any TMS.”

Putting this kind of structure in place and scaling back existing bank relationships is by no means easy, though. “There are all sorts of issues caused by the relationships, by local issues and by the inevitable teething problems with the new, more concentrated service. We have been in the fortunate position of being able to start with a very concentrated banking structure – even then, it is a challenge resisting all the ‘helpful’ suggestions emanating from various parts of the business about how we would gain by opening relationships with more local banks,” Glendinning observes.

But he also reiterates that “the more banks you have, the harder and more expensive it is to collect the data, and to effectively control the cash, once you know where it is. A tough stance may not win any popularity contests – but it certainly improves efficiency.”

Nevertheless, in today’s world, the counterparty risk exposure of working with a single bank provider is simply not an option for the majority of multinational companies – or for those with significant borrowing requirements. Running a multi-bank relationship spreads that risk, but also spreads your cash – making visibility more challenging.

“At this point, you really have to think long and hard about the relationships that you choose,” says Persson. “If you work with global or regional banks and use the partner banks in their network to cover your needs, this will give you better visibility than choosing individual in-country banks. Not only because there is more integration, but quite often you will find that the local banks who are not in some kind of alliance simply do not have the technology to provide the information that you need – whether that be SWIFT capability or a proprietary system.”

Cash management structures

Where some companies are prepared to invest in technology to improve their visibility, others cannot justify the expenditure, or simply see another way. Lenovo, for instance, has taken a largely structural approach to improving cash visibility and control. “We have done everything to keep the cash structure as simple as possible: by having a single account in each country, we have been able to avoid the dispersion of cash which is a major cause of lack of visibility,” says Glendinning. “Also, we operate a physical daily sweep of cash to our centre – this avoids having cash balances build up around the world except, of course, in countries with exchange controls.”

Moving cash to a single location, often the company’s home market, or to a given location that is favourable from a tax or regulatory point of view, is a technique that is commonly employed by companies looking to achieve visibility over their cash position on a per currency basis. This can be achieved by using an electronic banking system to initiate credit transfers, which is highly manual, or through an automated cash pooling solution.

Pooling: visibility and control

Here we stray more into the realm of cash mobility, than visibility, however the two are inevitable bedfellows when it comes to best practice liquidity management. In fact, the term ‘visibility’ is becoming almost synonymous with the double whammy of ‘visibility and control’. After all, as Persson puts it, “if you can’t control and mobilise the money, then the value of having visibility over it is vastly reduced.”

So how can pooling assist? While both physical and notional pooling can help to support improved real-time visibility and control over global cash positions, there are some important nuances to grasp. According to a recent whitepaper published by the Treasury Alliance Group consultancy: “Many companies are initially attracted to notional pooling because of its conceptual simplicity and the fact that much of the work is done by the bank. As corporate thinking evolves to include regulatory issues and price, physical pooling generally becomes the more preferred choice.”

While the whitepaper outlines several drivers for this preference, including the advent of the Single Euro Payments Area (SEPA) and the growth in enterprise-wide ERP adoption, another factor quoted in favour of physical pooling is that “virtually all cash is visible through web-based balance reporting solutions which allow treasurers nearly instant access to all accounts in the pooling arrangement.”

But for Mustafa Kiliç, former Head of Regional Treasury and Group Risk and Insurance Manager at a white goods manufacturer, the key to that statement is the word ‘virtually’. “We were operating in locations where it was extremely difficult to gain visibility, such as Russia.” Adopting one cash and liquidity management approach for all countries the company was operating in was simply not feasible. “Due to different rules and regulations some entities may not be permitted to participate in cash concentration or notional cash pooling agreements. This makes visibility very challenging, especially as the complex markets do not tend to have an advanced technical infrastructure in place,” explains Kiliç.

In conjunction with ING/Bank Mendes Gans, the company developed a hybrid cash pooling solution that would allow it a level of visibility and control that was not possible through physical or notional pooling alone. “Before we had the hybrid solution, we would be buying one currency, selling another and making inter-company loans. And if it was a significant amount of money, we would wait for the right time in the market to do the FX deal, perhaps as long as a week, meaning that even if the cash was visible, it was not reachable. The hybrid cash pool gave us instant access to our cash – as well as visibility, even in challenging countries such as Russia and Turkey.”

The technical details of this hybrid cash pool can be found on the Treasury Today website, as the solution was Highly Commended in the 2010 Adam Smith Awards in the Global Liquidity Management category. And for more information on physical and notional cash pooling techniques, refer to Treasury Today’s European Cash Management Handbook.

Reaching the next level

Beyond the three macro factors outlined above, there are numerous tips and tricks that companies can employ to improve their cash visibility. The relevance of these largely depends on each company’s visibility goals – and even definitions, however.

Persson, for example, believes that a useful tool for taking visibility one step further is electronic bank account management (eBAM). “It may not offer account visibility as such, but having control around account management processes, data and signatories makes visibility sustainable.” Indeed, some companies implementing eBAM have reportedly discovered bank accounts that they did not even know existed before – so this adds a completely new dimension to the visibility concept.

For others, valuable visibility tools include commercial cards – these are often linked with expense management systems, which help improve visibility as they offer treasurers the functionality to consolidate their indirect costs in one place, allowing for a more accurate review of transactions and overall expenditure. “This greater visibility of outgoings also enables treasurers to track trends, such as potential over-expenditure and spend with suppliers,” says Karen Penney, Vice President and General Manager of Global Corporate Payments at American Express. “Companies with a relaxed policy may find that in allowing their employees to select suppliers, they are missing out on the opportunity to negotiate preferential rates for their company. Armed with the data, they can then ensure they establish a sharper policy, and shape conversations with their teams about the use of expenses in their company more effectively.”

What is more, says Penney, consolidating expenditure into a centralised system also saves treasurers valuable time cross-checking data. “Hundreds of hours can be spent checking costs, and making and recording payments, whereas a card programme can alleviate this time burden through creating automated and therefore more accurate processes.”

Technology holds the answers

These two examples alone highlight that while there are structural and organisational solutions that undeniably help, there is nothing quite like technology and data to improve visibility; but that technology has to be centralised and fit-for-purpose. “Just make sure you’ve got the right technology and the right data, especially from your operations,” warns Skanska’s Müldner. Otherwise, it’s a case of ‘garbage in, garbage out’, which defeats the point of the exercise entirely.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.