A transparent and holistic framework supported by appropriate key performance indicators (KPIs) can enable accurate benchmarking and vast improvements in treasury efficiency. In this article we look at the latest methods of measuring your treasury function’s performance.

No longer the enigma

Treasury is no longer the enigma or ‘black box’ it once was. Transparency is now of utmost importance, not only in the management of risks and monitoring of controls, but also in calibrating the performance of the function as a whole. This new focus on visibility allows accurate benchmarking within each industry sector, enabling treasury departments to learn, share and adopt best practices.

Table 1: Top three KPIs in each treasury discipline

Discipline

No 1 KPI

No 2 KPI

No 3 KPI

Overall treasury efficiency

Cash visibility

Cost as percentage of total business costs

Cash pooling structures (eg number of countries/currencies included, % of balances pooled/swept)

Core cash management efficiency

Cash pooling structures (eg number of countries/currencies included, percentage of balances pooled/swept)

Cash visibility

Transaction error rates/cycle time taken to establish daily cash position/cash flow forecasting accuracy

Working capital management

Days inventory outstanding (DIO)

Days payables outstanding (DPO)

Days sales outstanding (DSO)

Liquidity management

Cash flow forecasting accuracy

Cash flow forecasting cycle time

Return on investment (ROI)

Bank relationship management

Overall level of banking fees

Number of bank relationships

Transaction costs

Risk management

Value at risk (VaR)

Commodity price risk

Mark to market

Funding

Refinancing risk

Annual debt maturity as a percentage of total debt

Banks in credit facilities

Balance sheet management

Net debt/EBITDA

Net debt/equity

Annual debt maturity as a percentage of total debt

Source: Treasury Today European Corporate Benchmarking Study 2011

With the treasurer now playing a more strategic role within the business, highlighting and improving the performance of the treasury department is paramount to the company’s success. In fact, treasury activities previously perceived as mundane have now been elevated to tasks of major importance in terms of delivering growth and a competitive edge. They therefore receive the full scrutiny of those at executive level.

Moreover, the repercussions of the economic downturn, notably the ongoing liquidity crisis and the drive for transparency, have brought to the fore critical areas that must be continuously running – visibly – at optimum levels. These include cash visibility, forecasting, funding and financial risk management, not to mention counterparty exposure analysis.

As such, treasurers are implementing a formal measurement framework, whether or not it is dictated from Board level, and are using a scorecard method built on appropriate KPIs and metrics to gauge productivity and encourage growth.

The 2011 European Corporate Treasury Benchmarking Study conducted by Treasury Today reveals that over 80% of corporates are already using KPIs to measure performance in at least one area of their treasury function. For overall treasury efficiency, the most widely used KPIs are noted as cash visibility and cost as a percentage of total business cost, but in other treasury disciplines, foreign exchange losses and counterparty limit breaches are also areas where metrics are frequently employed.

The table left identifies the top three KPIs used against each of the eight disciplines addressed in the Treasury Today Study.

Understanding the concept

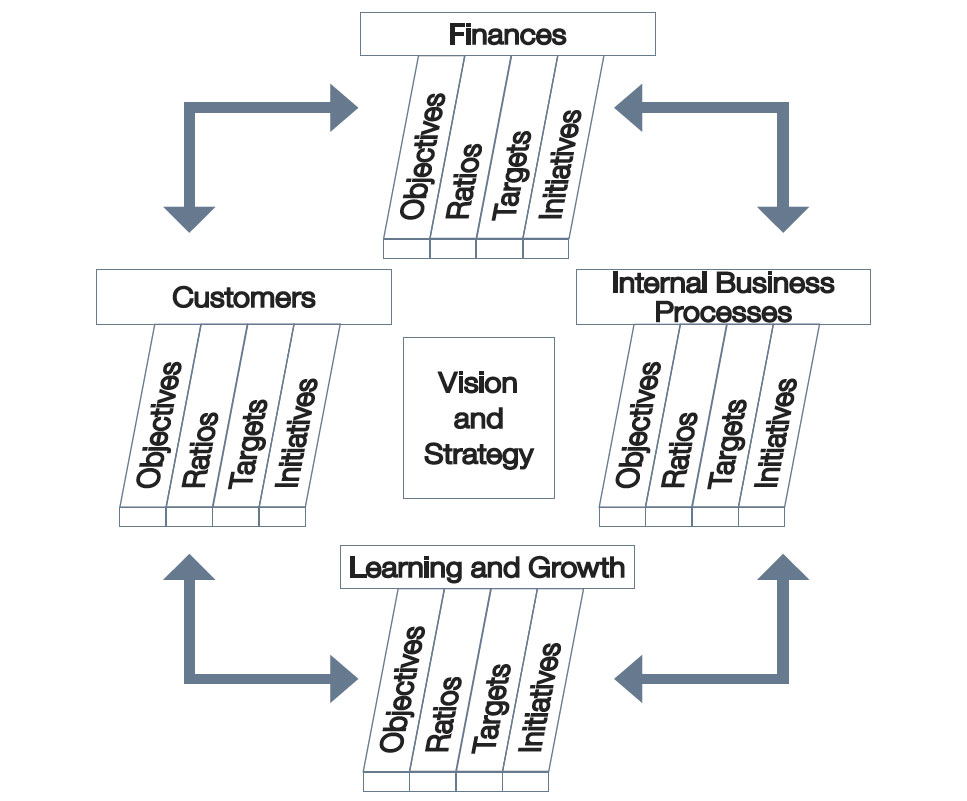

First conceived by Kaplan and Norton back in 1992, the balanced scorecard is a concept that embodies four ‘perspectives’ to provide the most holistic and transparent framework to optimise business growth.

The financial perspective is the measurement that is perhaps most naturally linked to treasury KPIs. There are three domain areas that apply to most corporate treasuries – cash management, foreign exchange (FX), and funding. Yet analysis cannot be made on financial data alone. The premise of the scorecard is that all four areas are explored to discern a true and balanced measure of business performance.

Measuring the development and self-improvement of employees allows managers to establish where training funds are most effectively allocated. Furthermore, a corporate can encourage the sharing of learning and best practice across the board, fostering the spread of shared corporate cultural values.

The function of treasury is the management of financial assets and liabilities and financial risk within an organisation – these are the internal business processes. Yet, in the simple management and execution of these processes, operational risk is created (ie through human error, system glitches, etc). There are a number of KPIs that are specifically used for measuring the efficiency of treasury processes and the performance of those processes in mitigating this operational risk.

Then there is the customer perspective. A positive result from customer satisfaction metrics can indicate future financial gains. But who exactly are the customers of corporate treasury? They are not only external – any internal unit or team or individual involved in the strategy and potential growth of the company is also a customer.

Of course, the traditional balanced scorecard does not suit every organisation in every way, and it must be tailored to the company’s business model and needs. For example, cash rich businesses will be more geared towards return on capital than diversification of funding and this will be reflected in their KPIs.

Automation of the balanced scorecard system adds structure and discipline to its implementation. It helps translate disparate corporate data into information and knowledge, communicate performance information and, ultimately, offers quick access to actual performance data.

Corporate treasury management systems are increasingly building in this scorecard functionality. This can help to eliminate the operational risk that stems from financial transactions by imposing key controls on the business processes within treasury (ie four eye principle on any new static data that is being used, second pair of eyes to authorise deals, authorisation panels on settlements etc.) They aim to give treasurers the tools to make their exposures visible and quantifiable; manage the financial instruments they are going to use; produce core reporting of cash and foreign exchange positions. The latest software also offers the functionality for performance reporting.

The integration and control that the latest software releases provide are specifically geared towards allowing treasury to operate in an integrated and efficient way. There are many balanced scorecard and/or performance management automation development companies. Some of the options are specifically dedicated to measuring performance management while others include tools which are designed for business intelligence, analytics or data warehousing, etc.

For example, within the software solution provided by IT2, the treasurer can access a library of best practice processes and key controls. That library applies across many treasury domain areas and has additional wide-ranging functionality, according to Patrick Coleman, Regional General Manager, IT2 Treasury Solutions. “The IT2 system also documents treasury procedures, with workflow functionality that can be used to drive the system. This is a highly sought after feature since Sarbanes–Oxley (SOX) was introduced and has matured in the last decade to accommodate other regulatory, accounting and operational reporting requirements.”

As suggested by the popularity of KPI usage in this area, a topical discussion in treasury at present is counterparty credit risk management. The origin of this for many was the debate around IAS 39 and the FAS 157 initiative in the US, which required corporates to adjust the market value of their assets to reflect counterparty credit risk. Pre-Lehman Brothers’ collapse, most people were using credit ratings to measure counterparty credit risk and learnt (the hard way) that they weren’t really an effective indicator – at least not in isolation.

Much of the latest technology now gives treasurers the capability to define their own counterparty credit ratings which can be based on default swap spreads or equity price volatilities, or any combination of those and anything else the treasurer chooses can be used as indicators. Those indicators can then be used to adjust the market value of the instruments and that then feeds through to management reporting and hedge accounting and counterparty limit policy and so on.

The successful adoption of balanced scorecard software from any of these providers will depend on whether the solution is easily accessible in terms of simplicity of use and in terms of company culture. A strategy map that communicates routine objectives clearly in familiar company ‘lingo’ will be most welcomed by employees across the organisation.

Rising to the challenge

An effective KPI programme underlying the treasury scorecard brings with it significant benefits, and more and more treasurers are jumping on board. However, adoption of this measurement method and its related technology is not without its challenges. We look at how corporates can address these potential issues:

The accurate selection of a relevant set of KPIs.

Too many metrics can be as detrimental as too few. However, the most important thing for corporates to remember is that they should always be appropriate to the business agenda. A third-party facilitator is often engaged to provide an unbiased view of the KPI selection and scorecard development process.

Strong technology support.

Collating, verifying, analysing and eventually generating valuable reporting on essential data requires a robust and modern IT infrastructure. A simplistic but powerful web based solution that requires minimal IT maintenance and operation will allow the balanced scorecard to integrate more effectively into the corporate. Sensitive introduction.Staff may feel slighted at the concept of performance measurement. Therefore, it is important to emphasise the end goal to employees – and the fact that it is generally the processes and not the individual that is being assessed.

Board level needs to be involved and aware.

These measurement standards are essentially treasury policy, which is set by the CFO or a risk committee. Therefore, while the treasury team has the responsibility of executing that policy, the executives need to understand the processes to enable accurate supervision of those processes.

Regular review of the scorecard framework.

To minimise disruption, an annual review is advised for most corporates once they have the flexibility to react to significant market developments as they arise.

Diagram 2: IT2 KPI Dashboard

Source: IT2

First launched in 2009, Treasury Today’s Benchmarking Study in association with J.P. Morgan, has evolved and expanded substantially, adapting to the feedback of industry participants in Europe, the Middle East, Asia Pacific and Latin America. North America is also being added this year. Our studies focus on the bigger picture and allow your company to compare its processes and attitudes with those leading the industry. During 2012 we will present our findings in Dubai, Singapore, US, Monaco, Brazil, China and at our European Benchmarking Roadshows in Dublin, Copenhagen, Stockholm, London, Brussels and Amsterdam.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.