Monitoring interest rates and acting on changes in them is an important part of a treasurer’s role. Whether looking at the yield on excess cash invested or the interest rate on outstanding or new issue debt, treasurers need to be aware of the impact of interest rate changes on the balance sheet and P&L and of the instruments and techniques available to mitigate the effects of those changes.

Interest rates can affect companies in several ways:

Companies with floating or variable rate debt outstanding are exposed to increases in interest rates, whereas companies with borrowing costs which are totally or partly fixed will be exposed to falls in interest rates. The reverse is true for companies with cash term deposits.

Pension schemes that carry liability and investment risk for the sponsoring corporation have interest rate risk in that liabilities act in a similar way to bonds, rising in value as interest rates fall and vice versa.

Although a nonfinancial firm will usually report its bonds on issue in financial statements, at substantially their face value, early redemptions must be done at the market value. This may be significantly different, as interest rates will change the value of fixed-rate debt.

How can it be avoided?

All of the issues above involve a decision to accept exposure either to a fixed interest rate or a floating rate on either an asset or a liability. This decision can be taken at any time over the life of a debt or an investment and can be modified at any time using a variety of instruments, some with an upfront cash cost, others with no upfront cash cost. It is also possible to purchase instruments that cap interest rates at a pre-defined maximum, floor them at a minimum or allow them to fluctuate within a pre-defined band or range.

Deciding to fix, float or accept a defined range of possible interest rates is the definition of managing interest rate risk. Hedging a floating interest rate means deciding to fix all or part of the exposure. Hedging a fixed rate exposure means deciding to transform all or part of it into a floating rate exposure. The following table lists the main instruments a corporate treasurer could use for this. It omits some less appropriate possibilities:

Tool

Description

Comment

Natural hedging

Creating interest rate exposures that are offset by elements of the company’s natural business cycle.

In normal times, for example, construction firms enjoy a rise in business activity when interest rates fall, as investors build more when the cost of projects is lower. Conversely, some firms may benefit from high levels of economic activity that prompt a high interest rate response by central banks.

Forward rate agreement (FRA)

An FRA is a tool for fixing future interest rates (or unfixing them) over shorter periods, up to say one to two years.

A 3v6 FRA allows a firm to fix the three-month Libor (or other reference) rate in three months’ time. It is dealt over the counter (with banks) and can be tailored to any (short-term) tenor.

Futures contracts

Futures have the same function as FRAs.

Futures are exchange-traded, have fixed tenors, terms and conditions, and require complex margining. They are therefore less flexible than over-the-counter instruments.

Exchange-traded options contracts

Interest rate options, bond options and options on fixed-income exchange traded funds are short-term instruments used to express views on whether rates will rise or fall.

Exchange-traded options have the same drawbacks as exchange-traded interest rate futures contracts. Over-the-counter options, such as caps and floors are preferred by most corporates.

Cap

An option that caps the interest rate payable by a borrower over its life. Below the cap level, the interest rate payable is floating.

Caps are dealt over the counter by banks. The commonest use is by borrowers who need to avoid covenant breaches that would be caused by sharp rises in rates and so purchase a cap to set the maximum rate they will have to pay over the life of a bond or loan.

Floor

An option that fixes the minimum interest rate receivable over its life.

Floors are dealt over the counter by banks. Treasurers with cash invested might buy a floor that is lower than current interest rates to set a minimum return.

Collar

A collar combines the purchase of a cap and a floor. This sets a corridor of possible interest rates between a maximum and a minimum.

A borrower would buy a cap and sell a floor, usually over the counter, thus creating a “collar,” or corridor, of rates. Usually the purchase and sale prices cancel each other out.

Interest rate swap

An interest rate swap changes the nature of a stream of interest payments from floating to fixed or vice versa.

Swaps are dealt over the counter and the market is large and deep. Maturities of anything from one year to 30 years are available.

Swaption

A swaption is an instrument where the buyer of a swaption has the right to enter into an interest rate swap as either payer or receiver of the fixed rate at a particular rate, thus protecting the buyer against adverse movements in long-term rates, while allowing him to benefit from favourable moves.

Swaptions are usually only used by non-financial firms in relation to a specific event such as a bond issue or an M&A transaction that will require funding.

Examples

The interest rate management tools most commonly used by treasurers are forward rate agreements, interest rate swaps and the option products caps/collars/floors. These instruments are flexible, customisable in terms of size, currency and maturity and are traded over-the-counter in large and liquid markets by the world’s largest banks.

Forward rate agreements

When two parties agree a price for an asset, to be exchanged at a set date in the future, they have agreed a forward contract.

In terms of interest rate risk, this is known as a Forward Rate Agreement (FRA). Corporates taking on debt purchase FRAs to hedge against the possibility of interest rates rising.

The corporate agrees to pay another party an agreed fixed rate of interest at the end of a given time period. Meanwhile, that second party agrees to pay the corporate a variable rate of interest over the same time period. At the end of that agreed time period the two payments are netted and one party receives a payment. As a result, the corporate buying the FRA benefits if interest rates rise, receiving a net payment from the seller of the FRA. The cost of servicing the initial debt also rises – a cost increase which is offset in whole or in part by the income from the FRA. The interest rate risk on the initial debt has been hedged effectively.

Conversely, however, if interest rates fall, the company would have benefitted from reduced interest payments. Some of that benefit is lost, as a payment is made to the counterparty in the FRA. The benefit of purchasing a Forward Rate Agreement, therefore, is that it reduces uncertainty caused by interest rate fluctuations, regardless of the way in which interest rates move.

Interest rate swaps

A swap is a derivative in which two parties agree to exchange a set of cash flows (or leg) for another set. A notional principal amount is used to calculate each cash flow; these are rarely exchanged by the parties. In an interest rate swap a fixed interest stream is exchanged for a floating stream (or vice versa). Each swap has two counterparties, and therefore in each swap one party pays fixed and receives floating, while the other party receives fixed and pays floating.

The swap rate at any given time is the fixed rate that a counterparty will accept in exchange for Libor. It is the fixed rate at which the present value of both the fixed and floating legs of the swap are, at the initiation of the swap, the same. (This explains why a liquid market can exist – at the beginning of the swap in theory both counterparties are indifferent as to which stream they receive and so the swap has no upfront premium). In practice swaps are used to express interest rate views and off-market swaps can be constructed using different fixed and floating rates. An interest rate swap can be viewed as a pre-packaged strip of FRAs.

There are two basic uses of swaps by non-financial corporates:

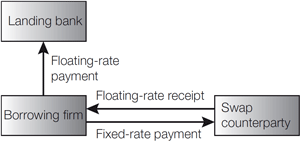

A floating-rate borrower converts to a fixed rate.

In this case a borrower has floating-rate bank debt and carries out a pay-fixed swap, converting the debt to a fixed rate. The two floating-rate streams cancel each other out for the borrower, leaving it to pay only a fixed-rate stream.

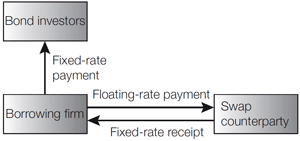

A fixed-rate borrower converts to a floating rate.

In this case a borrower has fixed-rate bond debt and undertakes a receive-fixed swap, converting the debt to a floating rate. The two fixed-rate streams cancel each other out for the borrower, leaving it to pay only a floating-rate stream.

So, for example, a company has taken out a floating rate €100m loan. To transform this into a fixed-rate liability it enters into an interest rate swap with a bank under which it agrees to pay the bank agrees to a fixed rate of, say, 5% over three years, and to receive a floating rate based on three-month Euribor plus 100 basis points. If Euribor is 5% at the start of the agreement, the fixed and floating legs are both 6% as the swap is initiated.

If Euribor rises to 6%, the floating amount payable by the bank to the corporate every three months is 7% of €100m divided by four. The company’s payment to the bank on the fixed leg will be less – 6% divided by four. The company uses the difference to pay the floating rate on its loan. Over the life of the swap the company continues to make variable payments on its loan and receives a net cash payment under the swap if rates rise, and makes net payments if they fall. In a fully-hedged transaction, these cash flows offset exactly the changes in the floating rate payments made to the company’s lenders and the net effect on the company is the same as if it had taken out a fixed-rate loan.

Caps, collars and floors

A cap is a derivative product in which the buyer receives payments at the end of each period if at the end of the period interest rates exceed an agreed strike price. For example, a borrower in danger of breaching banking covenants on interest cover if Libor rises above 4% could buy a cap with a strike price of 4% with a notional principal amount equal to the amount of their outstanding floating rate debt and with the same maturity as the debt, such that the buyer would receive a payment equal to any interest payments above 4%. As a cap is a series of interest rate call options, a premium is payable, usually upfront.

A floor is simply the opposite of a cap. The buyer receives a payment if rates fall below the pre-agreed strike price. The obvious user of this type of option is a depositor or investor.

A collar is the purchase of a cap and the sale of a floor. The long cap position sets a maximum interest rate payable. The short floor position means that the seller of the floor has to compensate the buyer if rates fall below the strike price. The effect of this is to create a range within which interest rates are free to fluctuate but if rates rise above the cap strike price, then the holder of the collar is compensated for that, and if they fall below the floor strike price, the holder of the collar must pay money to the floor holder. A borrower who has created a collar therefore pays a floating rate within the boundaries set by the two strike prices. Collars are usually constructed so that the sale of the floor cancels out the premium payable for the cap. The borrower therefore obtains zero premium protection if rates rise above the cap strike level but pays for that by taking the risk that rates will fall below the floor strike level. In that case the borrower will not benefit from that rate fall.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.