In the ever changing world of business, it is important to have support and insight from a trusted financial partner. Raising funding is now more challenging than ever before. Many treasurers are looking beyond straightforward bank debt and overdrafts, to consider a broader range of complementary solutions, which may include asset backed financing such as supply chain finance, trade finance, factoring, leasing and asset finance, as well as exploring debt capital markets and equity components.

Funding beyond bank loans

It would be difficult to talk about funding in 2010 without referring back to recent events that sent shockwaves around the world. Before 2008, many companies were accustomed to accessing the leveraged finance markets. For many corporates, there was little reason to look any further when considering funding options. In today’s uncertain economic climate, however, there is much to be gained by exploring a wider range of solutions.

Far from being unwilling to lend, many banks are working proactively to assist corporations by facilitating a more diverse approach to funding. Mark Stokes is the Managing Director of Lloyds Banking Group’s “Lloyds” Large Corporate division. Speaking to Treasury Today, he was keen to counter broad media criticism:

“My team is alive to the dynamics of UK businesses. We are working closely with our customers, understanding their needs and supporting them right through the cycle. In fact, we now have more relationship and business support managers across 24 offices in the UK, than we have had before. We are lending to create growth for our customers, and growth for the economy.

“You will not be surprised that we are working closely with the government too, and with the rest of the banking industry through the Business Task Force. We are as mindful as anyone of the important role we play in assisting the UK’s economic recovery. What we are not doing is lending for lending’s sake. That would be short-sighted and wrong, and no one would want that.”

The refinancing countdown

In early 2009, economic uncertainty in the funding markets prompted many corporates to refinance early. However, at that point final maturities were typically three years. As a result, a lot of companies will need to refinance again by early 2012 and many are looking to do so now.

Many of these companies are now willing to consider a wider spectrum of funding sources than before. These may include rights issues, US Private Placements and Eurobonds as well as bank debt. “Larger issuers have relied increasingly on the debt markets, and debt markets have gained importance relative to bank lending,” comments Robert Pierce, Managing Director, Head of ECM at Lloyds Banking Group. “Companies are also increasingly looking at equity.”

Although many providers have exited the lending market altogether, or have changed policies by sector, Lloyds has remained committed to supporting strong management teams. It aims to provide a full financing product suite. In this Product Profile we consider the alternative types of funding offered by Lloyds and explore how the funding markets are currently positioned.

Capital Structure Advisory

Lloyds provides financing solutions that often encompass a range of different products. In each case, the bank seeks to ensure solutions are appropriate for a client’s given circumstances and this desire to work proactively with clients at the earliest stage is manifested in the recently-established Large Corporate Capital Structure Advisory team which, as the name implies, provides corporate customers with a strategic analysis framework to help shape their funding strategy.

Lloyds’ Capital Structure Advisory is part of the bank’s Large Corporate relationship business, which looks after UK-based corporates with annual turnover above £15m, and typically up to £500m. In contrast to the Debt Capital Markets and Equity Capital Markets teams, which focus on particular product areas, the aim is to review, forecast and explore potential financing requirements at the earliest stage, before specific product needs are explicitly identified.

The purpose of the Capital Structure Advisory team is to provide a deeper and richer analytical capability to meet corporate clients’ increasing demand for forecasting, planning and front-end tactical discussions with their lead bank. From this a wide range of experts can be called in with practical advice based on financial projections and identified product requirements.

“Many clients were picking through the issues that surfaced as a result of the liquidity crisis, principally the economy swinging very rapidly into a recessionary mode and the impact of that on traditional corporate funding sources,” comments Michael McCartney, Director, Capital Structure Advisory.

“Equally, it should not be seen solely in the context of planning for the downside. Due to our close working relationships with good management teams, many of our clients are actually in very good shape. They have been managed well through the downturn and are in a good position to take advantage of opportunities in the market. This is another way our Capital Structure Advisory function can help clients by exploring tactical options which might be open to them due to the wider market conditions – in some instances, opportunities that haven’t appeared in decades.”

Forming the front end of planning, raising funding or refinancing, Capital Structure Advisory allows the Relationship team to act as a trusted partner, opening up strategic discussions with customers that typically focus on the following areas:

Evaluation of the client’s business, identifying key constraints as well as areas for growth.

Reviewing different funding solutions that could be employed to fulfil the client’s objectives, keeping credit lines open for when they are needed.

In conjunction with the credit team, early identification of the extent to which Lloyds is able to support the company in its chosen strategy going forward.

“A great testament to how we are adding value is the fact that many financial teams have turned around at the end of our meetings and asked for electronic copies of our analysis, so they can share the findings and strategic options with their board,” comments McCartney. “We are seen very much as part of our client’s advisory ‘team’ rather than simply a bank they can borrow from – they see professionals that can add material value to those strategic conversations they have internally every day of the week.”

Following on from the initial assessment and discussions, the Relationship team will then typically introduce finance teams to experts from particular product areas in the bank once a course of action is under consideration. When a product team has picked up the lead, Capital Structure Advisory steps back but continues to shadow the project, making sure that the eventual outcome meets the objectives that were set out in the opening discussions.

In terms of the funding strategies ultimately chosen by corporates, Lloyds offers a spectrum of options from straightforward loans to equity issuance. We explore these in more detail below.

General corporate lending

Summarising Lloyds’ strategy in the general corporate lending arena, Wendy Whewell, Relationship Director, comments: “We are here to support businesses through the cycle, ensuring that we understand the issues that they are facing and to work with our customers to find the most appropriate funding solutions.”

Under the heading of general lending, Lloyds offers a number of different products:

Asset based lending, including confidential invoice discounting, factoring and leasing.

Asset purchases via asset finance, for example vehicle funding and technology financing, which can be used to purchase certain types of computer equipment.

Traditional overdraft and term loan products.

Revolving credit facilities.

Trade and supply chain finance.

According to Mark Stokes, trade finance is up 40% year on year as dynamic businesses explore new markets for their products and services. “We are seeing more opportunities to bring a wide range of international risk management and trade finance solutions to corporates.”

In addition, Lloyds works with its corporate clients to look more widely at their businesses in areas such as carbon emissions where clients are looking for funding in order to replace vehicles.

Beyond these offerings, the relationship team is a conduit to dedicated product expertise, such as Debt Capital Markets, Equity Capital Markets, Financial Markets Risk Management, Lloyds Development Capital and other specialist product teams. Relationship management provides Lloyds Banking Group’s customers with an easy and practical route to a significant array of financing solutions.

Debt capital markets

The Debt Capital Markets (DCM) team enables its customers both corporate and financial institutions to access debt financing from the syndicated loan, private placement and bond markets. Rather than focusing on a specific debt product, members of the DCM team specialise by industry sector and provide expertise and lead transactions across a full range of products.

Syndicated loans.

Lloyds is currently ranked the number one bookrunner for UK Investment Grade loans. (Source: Dealogic)

US Private Placement.

Lloyds continues to deliver transactions on behalf of both debut and repeat issuers via its alliance with Bank of America Merrill Lynch, the long standing number one agent in the market.

Bonds.

Lloyds has invested heavily in its bond capabilities and has become a lead player in both investment grade and high yield sterling issuance. The build out of its European coverage continues apace.

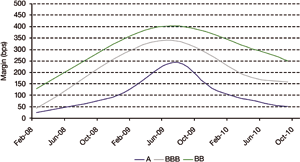

Chart 1: Loan Market Overview – Investment Grade

Source: Lloyds, Dealogic

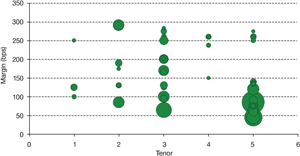

Chart 2: Loan Market Overview – Investment Grade

Bubble size relates to Deal size

The significant improvement in loan market conditions during 2010 has surprised most market commentators. “Competition for loan mandates is fierce again, which means that corporates are able to obtain facilities at tighter pricing and for longer tenors than was possible during 2009” comments David Cleary, Director, Corporate Debt Capital Markets. “If you are a strong multi-national corporate, then a five year maturity is now achievable on terms broadly in line with those seen in the market before the collapse of Lehman Brothers. This marked improvement will benefit corporates and enables bankers to underwrite M&A facilities with confidence.”

Meanwhile, the US Private Placement market is on course for a near record-breaking year in 2010 with around $40 billion to issuance. Cleary reports strong interest from UK corporates in this market. “This year we’ve seen companies dip their toes in to the market to explore investors’ reception to their name/sector as they seek to reduce reliance on the loan market for their debt financing. They’ve typically issued around $150-300m, with a view to going back at a later date as when other debt facilities mature.”

Despite a promising start to 2010 and favourable conditions for UK issuers, volumes in the sterling bond market are lower than 2009. This is in part due to low M&A activity and sizeable financings undertaken in 2009 by non UK corporates. “The markets are open and they’re crying out for supply from corporates, many of whom are currently watching from the sidelines. There is unmet investor demand and we expect a strong pipeline, particularly from high yield issuers in 2011,” comments Cleary.

In addition, Lloyds recently issued its own £75m retail bond that is quoted on the LSE’s retail bond platform. The expertise acquired during this process is being deployed to help corporate customers, particularly those with strong consumer recognition, to diversify their sources of funding and tap into pent up demand from retail investors.

Equity capital markets

“Today the FD is going to have to look at a funding solution rather than a product,” says Robert Pierce. “The solution is going to encompass multiple products. And one of those products is likely to be equity, because the only way to keep your leverage under control is to have enough equity on your balance sheet.”

Lloyds provides advice and executes primary and secondary equity issuance as well as equity private placements. The services provided by the equity team can be summarised as follows:

Market intelligence

Analysing the risk appetite available in the marketplace and understanding what the markets are willing to do in terms of providing equity funding to any given issuer.

Expert advice

On the equity component of the client’s financing solution and how it should be structured.

Underwriting rights issues.

“Our clients appreciate the value of associating our name to their transactions; it is a reassuring signal to the investor community in terms of the balance sheet commitment that the bank is providing to an issuer,” says Pierce.

The equity team typically works with clients which are either looking to strengthen their balance sheets in order to support the business through a difficult period, or which are looking to finance growth, both organic and by acquisition. “We are seeing a shift from the recapitalisation repair of the balance sheet type transactions, which we saw a lot of last year, to companies that are looking to take the business to the next step, contemplating making an acquisition outside of the UK or into a different sector – in other words, taking advantage of the opportunity,” says Pierce.

Overview of the equity markets

The IPO market so far in 2010 has been variable. Some public offerings have been successful, with others less so. A number of scheduled IPOs have been postponed or delayed because it was felt that the market was not ready for them.

“Investors have shifted their interest from the FTSE 100 to FTSE 250,” comments Robert Pierce. “Investor appetite has also shifted from helping corporates rebuild their balance sheets to helping companies to fund growth. But there is no certainty.”

“In the current market, we recommend to our customers to think about their strategy very carefully. They need to make sure that what they are planning to do is completely consistent with the strategy they have announced and with the key drivers of their business.”

“Another point is that these windows of opportunity open and close. Corporates need to be very well prepared and ready to pull the trigger on a transaction when the time is appropriate. It’s a combination of doing enough homework and communicating with investors.”

Outlook for 2011

Across the industry there is continuing uncertainty regarding the likely direction of the funding market in 2011.

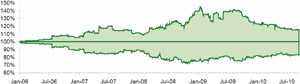

“There continues to be a lot of uncertainty with respect to the future,” says Robert Pierce. “If you go back to 2005 or 2006, I would say that on average, earnings forecasts for the FTSE 100 one year out were within a 5-10% range from the median. Today, earnings forecasts for the FTSE 100 are within a 20% range, or maybe more, on either side of the median. That tells you that we just don’t know where the economy is going.”

The range of analyst expectations for FTSE100 earnings remains wide:

Chart 3: FTSE100 Analyst earning estimate spread

At the time of writing, Cleary comments “the loan market outlook for 2011 is one of ongoing strength and stability with fierce competition for lead mandates likely to prevail. However, there could be a shock within the Eurozone that would have far reaching consequences across the bank market. The US PP market has been a relative safe haven for investors during the financial crisis and we expect the current favourable issuance conditions to continue in 2011. Bond issuers will continue to look for relative value across the main dollar, euro and sterling markets and, assuming that Sovereign risk does not increase, the technical mismatch between low corporate supply and strong investor demand will result in the bond markets remaining open for issuers.”

“It will still be a tough year,” adds Wendy Whewell. It is worth noting that more businesses fail coming out of recession than going into recession. This is because there is a greater demand on business’s cash as they seek to make the most of the opportunities that are coming their way from either new contracts or competitors that have failed. It is important that businesses manage their cash and balance sheets to ensure that they can fund this growth.

In the context of continuing uncertainty, and with treasurers now willing to look beyond bank debt in order to meet their funding needs, there is likely to be continuing strong demand for a wider range of funding strategies and for advice which will help them to navigate the changing landscape. As such, the suite of funding solutions offered by Lloyds is well positioned to meet corporate treasurers’ needs.

Lloyds Banking Group

Lloyds Banking Group’s corporate business provides comprehensive expert financial services to businesses ranging from privately-owned firms to multinational corporations and financial institutions. As well as offering the expertise and capabilities our clients need to compete successfully in the marketplace, we are proud of the relationships we build with our customers. We work closely with them to understand their business and offer the best financial solutions to meet their distinctive needs.

The wide range of services and innovative solutions we can deliver includes;

dedicated relationship banking;

capital market funding;

debt and equity finance;

treasury and risk management services;

structured finance solutions;

asset finance;

leasing;

company registration and employee share schemes;

competitive e-trading facilities.

import and export trade finance;

tailored cash management solutions; and

structured credit investments and securitisation facilities.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.