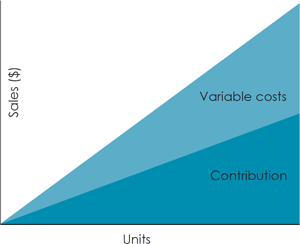

Contribution margin is a measure of profitability that evaluates the percentage of sales revenue remaining after variable costs have been deducted. Variable costs should include the cost of raw materials or shipping, for example. These are as opposed to fixed costs, such as rent or salaries. The contribution margin may also be used to determine the profit margin of each unit of a particular product or service.

Diagram 1: Contribution margin

How is it calculated?

Contribution margin is expressed as a percentage and can be calculated using the following formula:

Company XYZ had sales revenue for the 2009 tax year of $81.4m and its variable costs for the year were $52.4m. Company XYZ’s contribution margin for the 2009 tax year is therefore:

Company XYZ has two major products – Product A and Product B. The product revenue generated from Product A over the 2009 tax year was $48.7m and for Product B it was $33.2. The variable costs for producing Product A and Product B were $30.0m and $19.1m respectively. The contribution margin for each product was therefore:

These figures show that both Product A and Product B have contribution margins that exceed the contribution margin of Company XYZ as a whole. This might suggest that the company’s smaller product lines are dragging down the company’s overall performance. Product B’s contribution margin is greater than that of Product A, illustrating that the variable costs of producing Product B are proportionately lower. In addition, Product B may have a greater margin priced into it when it is sold on to the consumer.

Points to consider

Contribution margin may be used to identify products that are underperforming. If a product’s contribution margin is falling short of the company’s contribution margin, it may be worth investigating whether the fixed costs of producing the product can be reduced, whether the product’s sale price could be increased or whether the product should be removed from production altogether.

Contribution margin is sometimes confused with gross product margin. They are not the same, however, since gross product margin only takes into account the cost of sales (or cost of goods sold), whereas contribution margin uses the total variable costs. When using this ratio to compare, between products or companies for example, it is important that the same costs are included in both calculations. For instance, some sales costs may be regarded as fixed, others as variable.

Join our global community

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.

Creating a free account helps us to understand our community better, and tailor our content and events to suit your needs. You can unsubscribe at any time.