Global treasury management – taking an end-to-end approach

Published: Sep 2007

The global economy has shown great resilience in recent years despite rising oil prices and several natural disasters. Growth in the US, Japan and the Eurozone averaged 2.4% in 2005, down from 2.9% the previous year. In stark contrast Asia and other emerging markets have continued to grow at a breathtaking pace (see Figure 1 below). Growth in market liquidity and interest rates close to all-time lows has resulted in greater M&A activity and higher rates of investment on a global basis. Controls on foreign ownership have been relaxed in several Asian markets including, importantly, China, as a means of encouraging inward foreign direct investment (FDI). Aggregate gross domestic product (GDP) for Asia expanded by a robust 7.4% in 2005 led by China and India. Demand for emerging markets output is expected to remain very healthy in this current business cycle. This has had a dramatic impact on the treasury management arena as corporations continue to move their focus to these emerging economies in search of new business and profits.

This new environment is therefore driving rapid change within the finance function. The natural expansion of the treasurer’s role beyond its traditional bank balance and transaction management responsibilities is being accelerated further. Rapid growth in the emerging markets is placing even greater demands on the treasurer, as trade flows are now required to be managed in countries and currencies hitherto considered ‘exotic’. Their impact and importance is, quite simply, too great to be ignored. The liquidity upheavals this summer have heightened the importance of effective global treasury management and optimisation of internal liquidity. The dynamics are shifting on a number of fronts and the issues faced by corporate treasurers are as challenging now as they have ever been.

In this Business Briefing we assess the new challenges faced by the treasury department, the drivers of globalisation and the benefits which can be achieved through an ‘end-to-end’ approach to treasury management on a truly global basis.

Figure 1: World GDP % growth rates

2005

2006e

2007f

OECD Countries

2.6

3.0

2.3

Euro Area

1.4

2.4

1.9

Japan

2.6

2.9

2.4

United States

3.2

3.3

2.1

Non-OECD Countries

5.8

5.3

4.7

BRIC Countries

Brazil

2.3

3.5

3.4

Russia

6.4

6.8

6.0

India

8.5

8.7

7.7

China

10.2

10.4

9.6

Source: World Bank e = estimate, f = forecast

Drivers of globalisation within the treasury function

The increasing globalisation of business, together with a geographic and market shift towards increased volatility is leading companies to devote greater attention to cost and risk with a view to improving cash management processes. In particular, many companies are now actively evaluating the pros and cons of moving to globally centralised models for an increasing range of functions, taking an ‘end-to-end’ approach to treasury management.

These companies focusing on global treasury management, often share the following characteristics:

Fast growing.

Large proportion of business conducted in rapid growth emerging markets.

Receptive to fast organisational evolution.

Management culture open to speedy decision making and quick implementation.

The trend towards end-to-end global treasury management is leading some companies to re-evaluate the fragmented banking approach, as globalised banking models can yield substantial scale economies.

Such companies are now explicitly evaluating a trade-off of treasury centralisation versus reciprocity of banking services for credit extended and there are cost implications to consider of slicing the cake differently. As only a handful of service providers can offer these truly global treasury solutions, corporations now have to find alternative means of rewarding those banks which provide credit and yet are currently relatively limited in their offering of globalised banking solutions.

Rather than following the tried and trusted models of country first, then regional overlay, some companies are making step-change transition straight to a truly global model. We are also witnessing an increase in this consultative/advisory type approach rather than banks merely being asked to respond to the more traditional request for proposal (RFP) process of buying banking services.

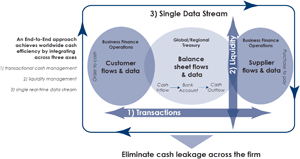

This approach requires an entirely different mindset to achieve the desired end result from the vision through to optimisation of the benefits. This is new territory for many companies and they are now seeking advice on how to go about this global journey and how to adopt an entirely new operating model (see Figure 2 below).

Citi’s recent experiences working with clients suggest companies are also re-defining the role of treasury to be much more strategic rather than merely transaction execution. For example, a large global electronics company recently approached Citi with a request to prepare a ‘White Paper’ on ‘How to create an effective global treasury function’. Banks have a role to play in helping the treasury department achieve its strategic aims as well as providing the traditional banking products and services.

Figure 2: End-to-End (E2E) Treasury Approach

As companies move their focus away from deregulated markets where cash management is relatively simple, to regulated emerging economies such as the BRIC countries (Brazil, Russia, India and China), so the challenges get tougher. Such markets have intrinsic volatility and are growing at a rapid pace so the requirement to maintain an effective and standardised control mechanism is even more crucial.

Technology is obviously a key driver in this space and treasury departments have to leverage automation to the full. Companies need a clear global technology strategy as they wrestle to undertake more and more both in quantity and complexity with flat or, worse still, reduced headcount. The aim is to establish a single real-time data window onto an increasingly broad business empire.

An end-to-end approach = visibility, control and optimisation

By taking such an end-to-end approach, corporate treasurers will be able to realise measurable improvements in three key areas;

Visibility.

Control.

Optimisation.

Visibility

Over time as market intensity increases it becomes increasingly important, particularly so during times of volatility, for treasurers to be able to access information where they want it, when they want it and in a format that is easy to understand and act upon quickly. The trend is moving away from such data being based on weekly or monthly cycles, to daily and even real-time multi-bank information feeds. This is laying firm foundations for companies seeking to improve the control and optimisation of their liquidity on a global basis, and reducing amounts of liquidity remaining trapped or even unmonitored.

In some cases, apart from the market and competitive drivers mentioned earlier, there is also a regulatory impetus for improved data visibility, such as Sarbanes-Oxley. This particular requirement is driving companies to recognise the importance of the treasury function and encouraging operating units and subsidiaries to provide central treasury with information in a timely, accurate and consistent manner.

Furthermore, this requirement is driving improved sharing of data through common standards. There is also increased recognition that cash is an asset which can be utilised far more effectively if the central treasury function knows about it and is able to have effective dialogue with business units from sharing a single common data view.

Currently, many companies derive this data view from large ERP and / or TMS solutions. However, these can be expensive and time-consuming to change or update and are not always easily accessible to business units. Information exchange between central treasury and operating units should be based on robust yet scalable platforms, such as Citi’s TreasuryVision, which can be shared across the enterprise and work alongside the more functionally rich ERP / TMS systems. Such emerging infrastructures are enabling treasurers to add value far beyond the historical treasury boundaries.

Control

We highlighted earlier the importance of emerging markets on cash management structures as overall liquidity growth slows down. It is therefore essential to establish a robust control environment. This includes standardising treasury policy and procedures and risk management frameworks to accommodate business expansion in a diverse range of markets. The ability to understand risk profiles better will help corporate treasurers in terms of working capital management and the company’s balance sheet.

The demand to analyse volatility on a real-time basis is fuelled by a greater understanding of risk exposure and scenario modeling and we will start to see a wider range of products being introduced by service providers. Spreadsheet-based tools will decline in favour of integrated web-based solutions providing much higher levels of accuracy, automation, workflow management and, importantly, security.

Cash flow forecasting is one area where we expect to see improvements in the solutions offered and these will be integrated with the liquidity solutions.

Optimisation

The developed markets around the globe facilitate a range of funding choices. The challenge for treasurers when global liquidity structures are established is how to optimise surplus liquidity automatically within such global structures. It is relatively easy to mobilise and transfer working capital within the developed markets. SEPA is an example of deregulation that will further facilitate funds transfer within the EU.

However, this is in stark contrast to the completely different landscape in the emerging markets. These countries are still highly regulated or deregulating at a much slower pace than the EU and US which, therefore, restricts funding choices. The tools and techniques used by corporate treasurers in the cash management space in the developed economies are not easily replicated in the emerging markets, although we are seeing new solutions emerging, such as interest optimisation.

Case Study

LG Electronics

S. H. Koo

Global Treasurer

A global electronics manufacturer with 82 subsidiaries across four core businesses, LG Electronics historically supported subsidiaries’ cash processes through a network of regional treasury centres. However, in 2005, the company decided to establish a global treasury centre to achieve a more coordinated, end-to-end approach to cash and liquidity management. “We wanted to reduce interest costs and the various bank fees. Also we wanted to optimise cash balances, and establish common processes that would leave subsidiaries ‘cash free’ and able to concentrate resources on core tasks. Furthermore we needed greater visibility over the global daily cash position.” says S. H. Koo, Global Treasurer, LG Electronics Inc.

LG Electronics’ first step toward standardisation and centralisation was to replace local bank-supplied systems and manual cash processes with the installation of a global treasury management system. Its global treasury centre was established as an in-house bank which both centralised inflows from subsidiaries and initiated external payments on their behalf, thereby introducing common processes across the firm. Following a benchmarking project and RFP, Citi was selected to support the new treasury structure and implement a global multi-currency notional pool to consolidate liquidity at Citi’s London branch. Starting in Q4 2006, funds are swept automatically on an end of day basis from subsidiaries’ target balance accounts to corresponding treasury accounts in London for notional offset. Balances at third-party banks are automatically swept via a SWIFT message-based platform. This structure includes 41 subsidiaries from 23 countries and now pools balances denominated in 12 currencies. Besides this structure, LG Electronics has a separate pooling structure in China (16 subsidiaries, two currencies) for regulatory reasons.

Citi is able to provide its multi-currency notional offset offering through an interest-parity framework which replicates the benefits achieved through FX swaps. While notional pools have typically consolidated excess liquidity in a single currency, eg in EUR or USD, LG Electronics has been able to incorporate cash flows in many more currencies (including HUF, PLZ, CZR) in a single ‘pot’, thus capturing a much larger percentage of surplus funds for investment or balance sheet purposes. Importantly, because the end-of-day multi-bank TBA sweeping process is fully automated, the administrative burdens of liquidity management are minimised while the scope of the pool is increased to a truly global level.

In addition, to improve control and visibility of newly-standardised transaction flows, the firm established a global payment factory with Citi and two other banks that consolidates all payments from subsidiaries into a single file which is then forwarded to these banks for routing and execution. To complete the transaction cycle, payment reconciliation data and balance information on all treasury and subsidiary account balances is provided into LG Electronics’ treasury management system, which enables the firm to generate accounting entries automatically.

From transaction execution to liquidity management through to control and reporting, LG has implemented a streamlined, end-to-end treasury structure which has achieved the firm’s objectives, while also creating a platform for future efficiencies. As well as interest savings through cash optimisation and improved cash flow forecasting through greater visibility, cost reductions have accrued from common processes that have increased automation and reduced banking interfaces. “Only now that we are following common processes company-wide, we can make decisions – such as our use of communications networks – based on a global strategy. Moreover, we work more effectively with the businesses, because we’re all using the same processes and tools,” says Mr. Koo.

However, the choice to establish a global treasury management structure is not taken lightly and the company’s board will expect an attractive return on investment (ROI). For this reason, those banks operating in this space are devoting far more time now in assisting companies with the cost/benefit analyses and in justifying the internal business case to proceed.

One means of doing this in respect of a cross-currency liquidity structure is to analyse the mix of currency balances over a period and work out the cost of converting the basket of currencies to a base currency using swaps. This very often provides a very visible and compelling argument to support the business case.

Regional liquidity structures have been common for a while for global currencies such as USD and EUR, and in some cases these currencies have been managed on a global basis. We are now seeing the emergence of cross-currency structures such as multi-currency notional pools, which are creating an entire new set of possibilities for corporate treasuries to partner their business units as well as broaden coverage of the corporate balance sheet. Banks have also started developing solutions covering more regulated markets, such as cross-border interest optimisation structures which can function on a stand-alone basis, or integrated with a global liquidity structure.

The end-to-end approach referred to earlier is complemented with a focus on the investment of net surplus funds. The primary purpose of managing the company cash on a global basis is to avoid the need to go to external sources for funding.

As market liquidity tightens, it is more important than ever, that companies make their surplus cash work harder through the right investment choice. Money Market Funds, long popular in the US, are emerging globally as an increasingly popular shortterm investment asset class.

On-line portals which allow access to all balances instantly are on the increase and it is important to have access to a sufficient number of counterparties and asset classes via on-line investment portals to ensure an appropriate portfolio mix. Furthermore, once investments have been executed, the portals should provide reports on balances and current yields quickly and accurately on a daily basis, as well as enhanced analytics such as portfolio yield and performance against pre-determined benchmarks.

Another route being increasingly explored is the concept of ‘drain the pool’ automated investments, where liquidity structures are linked to investments through automated rules based on treasuries’ investment policies, ensuring investment decisions are optimised.

Benefits of a global approach to treasury management:

Helps to address the legacy of multiple bank accounts and technology platforms.

Services not necessarily tied to credit anymore.

Time zone differences overcome.

All-inclusive currencies.

Improved decision-making.

Cost savings.

Investment opportunities improved.

Enhances control.

Reduction in interest cost.

Process efficiencies.

Visibility of information.

Company credit rating improved.

Fosters a culture of cross-business dialogue and co-operation.

Conclusion

Corporate growth has been increasingly shifting towards faster growing but volatile emerging markets, particularly the BRIC economies. We are also seeing a marked change in liquidity; the benevolent environment of recent years has become significantly more inclement, with the verdict still out on how broadly the contagion spreads.

This transition is shifting attention to step change efficiencies across the enterprise with the finance function rapidly moving to centre of plate, as the premium on access to liquidity increases, and fully utilising internal liquidity becomes increasingly paramount. Treasurers’ workloads have been increasing in terms of both quantity and complexity as increasing business demands outpace resources available. Couple this with the trend towards doing business in new and often volatile markets across different time-zones and the finance function’s challenges are measurably more difficult than ever before.

It is only by taking an end-to-end approach to global treasury management, that corporate treasurers will be able to satisfy the conflicting demands of efficiency and control, constrained resources, as well as scalability and flexibility for growth. Fortunately, this increase in demand for end-to-end treasury solutions is starting to be met by global banks.

Those with extensive country coverage and global technology platforms are well placed to respond to this growing global trend. We could therefore start to see a fundamental change in the treasury management marketplace within the corporate and service provider universes in the next few years as the market evolves to the next stage.

Citi

Citi Markets & Banking is the most complete financial partner to corporations, financial institutions, institutional investors and governments in the world. As a global leader in banking, capital markets, and transaction services, with a presence in many countries dating back more than 100 years, Citi enables clients to achieve their strategic financial objectives by providing them with cutting-edge ideas, best-in-class products and solutions, and unparalleled access to capital and liquidity.